Housing Prices in Buenos Aires: Slowing Growth

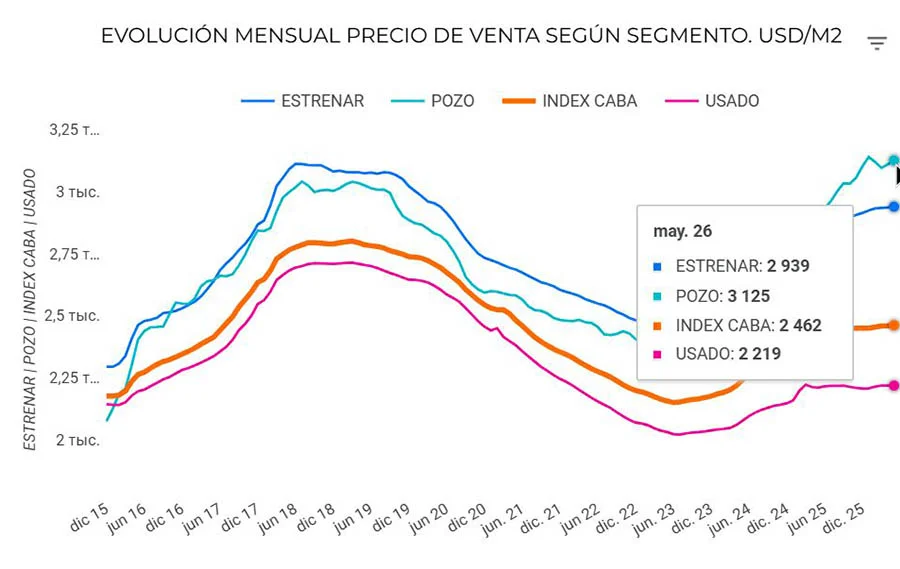

The real estate market in Buenos Aires has shifted into a phase of price stabilization after several years of strong growth, according to a study by the Zonaprop portal. Current levels remain roughly 12% below the historical peak. Overall, average apartment prices have largely stagnated, although in some districts annual growth still reaches double digits.

Apartment Price Dynamics in Buenos Aires

In May 2026, the average listing price of apartments in the capital rose by just 0.1% compared to April, reaching $2,462 per square meter. Compared to the same period in 2025, the increase was only 0.6%.

One of the key indicators of changing market conditions is the decline in the share of districts showing monthly price growth. At the end of 2022, only 20% of neighborhoods recorded increases, but this figure steadily rose to 90% in June 2024 and remained at that level in early 2025. The trend then reversed: by May 2026, only 52% of neighborhoods showed positive monthly dynamics.

The average price of a 40 sq. m studio is estimated at $108,377, a 50 sq. m two-bedroom apartment at $130,391, and a 70 sq. m three-bedroom unit at $179,389. These are listing prices rather than transaction values, but they remain the standard benchmark for monitoring market sentiment.

Price Dependence on Construction Stage

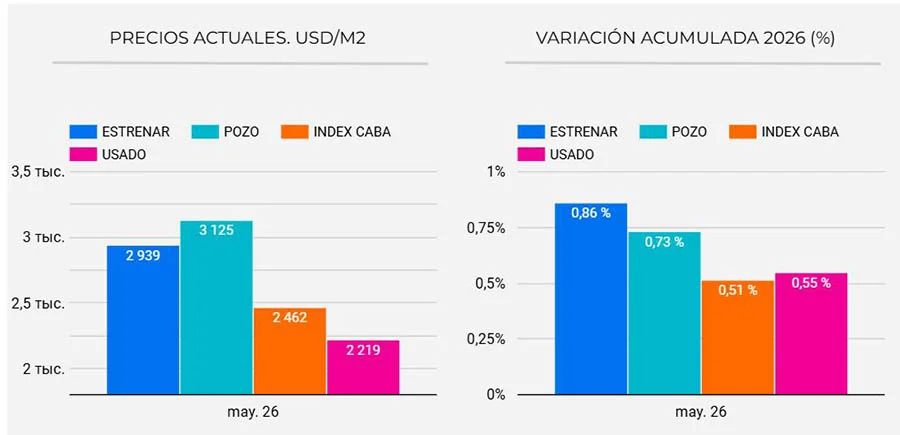

The most expensive segment remains pre-construction (“under construction”) units, at $3,125 per sq. m. Newly completed properties are priced at $2,939, while the secondary market remains the most affordable at $2,219. This gap reflects a persistent premium for early-stage developments and a lower valuation of already occupied housing.

As a result, the traditional price hierarchy in the city remains in place, where early-stage projects command higher prices than completed units. The overall market index (CABA) stands at $2,462 per sq. m.

Price dynamics across segments remain synchronized and weak. Since the beginning of 2026, growth rates are broadly similar: new completed apartments rose by 0.86%, pre-construction units by 0.73%, the secondary market by 0.55%, and the overall city index by 0.51%. This points to a lack of a clear growth driver in any segment.

Leading and Lagging Districts by Apartment Prices in Buenos Aires

Apartment Prices

In five districts of Buenos Aires, apartment prices recorded the strongest growth. Saavedra leads, with prices rising by 10.1% to $2,862 per sq. m. Parque Avellaneda follows with a 9.5% increase to $1,660. Agronomía ranks third with growth of 6.4% to $2,240. The top five also include Parque Chas (+5.24% to $2,449) and Santa Rita (+5.13% to $2,139).

The sharpest declines were recorded in Lugano, down 4.83% to $1,041 per sq. m. In Constitución, prices fell by 4.02% to $1,838, and in San Nicolás by 3.99% to $1,796. Paternal (–2.11% to $2,045) and Villa Luro (–2.03% to $2,120) also saw declines.

Houses in Buenos Aires

Among houses, Constitución recorded the strongest growth, up 27.43% to $1,087 per sq. m. San Telmo rose by 13.44% to $1,588, and Parque Chas by 13.17% to $1,796. Núñez (+11.30% to $2,252) and Chacarita (+10.06% to $1,886) also showed increases.

The opposite trend was observed in La Boca, where prices dropped 22.06% to $648 per sq. m. Floresta declined by 8.57% to $1,207, San Nicolás by 5.12% to $1,187, Flores by 4.80% to $1,196, and Parque Patricios by 4.10% to $983.

Key Locations and Investment Price Benchmarks

The Buenos Aires real estate market in 2026 maintains a clear price hierarchy across districts and property types, shaping different entry strategies from premium to budget segments.

Premium Segment

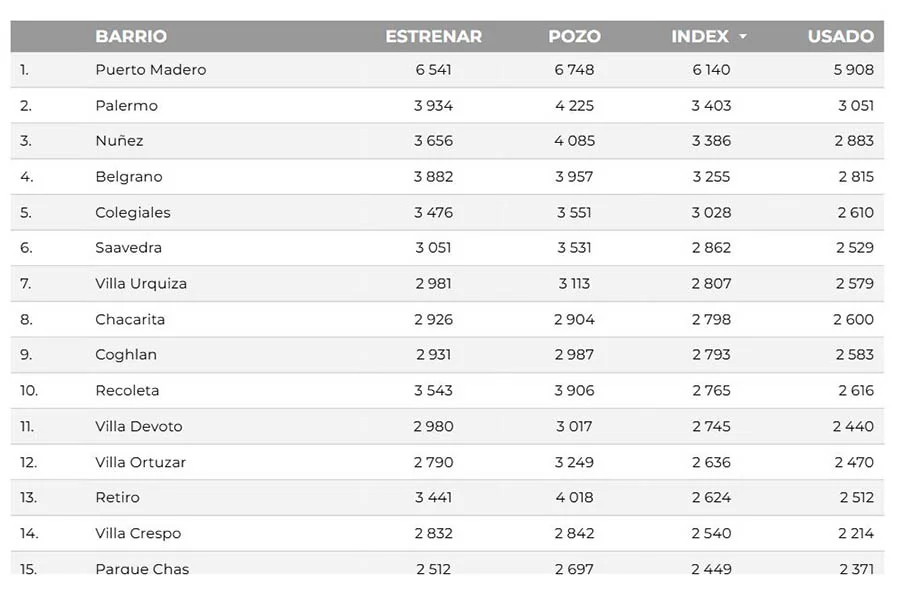

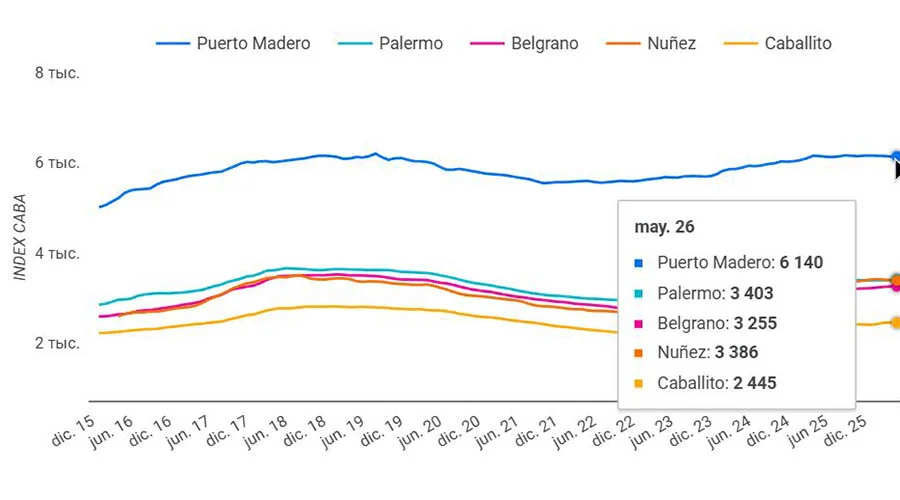

Puerto Madero remains the most expensive district, at around $6,140 per sq. m. In new developments and pre-construction projects, prices exceed $6,500, while secondary market values remain above $5,500 per sq. m. This segment is characterized by high capital concentration and stable pricing.

Palermo maintains steady demand in the premium-mass segment, averaging around $3,403 per sq. m, with higher prices in new projects and lower values in resale units.

Nuñez and Belgrano show similar dynamics, with a range of $3,200–$3,400 per sq. m, stable demand, and strong liquidity driven by residential and family-oriented demand.

Caballito is positioned in a more balanced range at around $2,445 per sq. m. The gap between primary and secondary markets is present but less pronounced than in premium districts.

Budget Locations

In the southern part of the city, price levels are significantly lower. In Nueva Pompeya, the average price is about $1,459 per sq. m, while resale values are around $1,272. Villa Lugano remains the most affordable area, at roughly $1,041 per sq. m on average and below $1,000 on the secondary market.

Conclusion

Analysts at International Investment note that in 2026 the Buenos Aires real estate market does not show broad-based price growth, reducing the effectiveness of investment strategies focused on overall market appreciation. In this environment, assets with proven demand become more important, offering more predictable liquidity and rental potential. Properties in districts with negative price dynamics tend to have longer exposure times and limited scope for price appreciation.

The Argentine real estate market is also seeing a decline in investor interest, with capital shifting toward alternative financial instruments. This has changed demand patterns and pushed developers to focus on end-users. As a result, developers are moving away from small investment-oriented rental units and returning to residential housing for end consumers.