Lithuania Prepares New Curbs on Russians and Belarusians

Lithuania Prepares New Curbs on Russians and Belarusians

Singapore Keeps Forest Sites in Housing Pipeline

Singapore Keeps Forest Sites in Housing Pipeline

Cheap Flights Could Disappear as Airlines Turn to AI

Cheap Flights Could Disappear as Airlines Turn to AI

Vilnius Expands Supply as Home Prices Keep Rising

Vilnius Expands Supply as Home Prices Keep Rising

Kazakhstan plans to introduce electronic entry permits

Kazakhstan plans to introduce electronic entry permits

Czech Property Investment Accelerates in Second Quarter

Czech Property Investment Accelerates in Second Quarter

Tbilisi Housing Market in 2026: Slowing Price Growth and Declining Returns

The Tbilisi housing market remained highly active in the first quarter of 2026, according to a TBC study. Transaction volumes continue to grow, prices are still rising but at a more moderate pace, and demand remains stable. At the same time, signs of structural cooling are becoming more visible: rental rates and returns are declining.

Q1 2026: Divergence Between Segments

In Q1 2026, the volume of Tbilisi’s residential real estate market reached $941 million, up 24% compared to the same period in 2025. A significant contribution came from the completion of major development projects, which helped boost overall figures.

The number of transactions also showed steady growth. A total of 10,723 apartments were sold (+19%). The average asking price reached $1,343 per sq. m (+6%), although growth rates have noticeably slowed compared to previous periods, indicating gradual stabilization.

The gap between market segments remains substantial. Over the past 12 months, average sale prices were $4,169 per sq. m in the Luxury segment, $2,869 in Upper Premium, and $2,126 in Premium. In the mass market, levels are significantly lower: Comfort at $1,465, Economy+ at $1,092, and Economy at $803. As a result, the difference between the highest and lowest segments exceeds a fivefold gap, reflecting uneven demand and differences in purchasing power.

Housing Transactions in March 2026: Shift Toward the Secondary Market

March 2026 was one of the most illustrative months. The number of transactions reached 4,031 (+32%), while total volume increased by 33% to $352 million. The average transaction price rose by 4% to $1,341 per sq. m. At the same time, the average asking price fell to $1,011 per sq. m, down about 5% year-on-year.

The market structure is clearly shifting toward secondary housing. In March, sales of new apartments declined to 564 transactions (-3% YoY), reducing their share of total sales to 14%. In contrast, resale apartments increased to 3,467 transactions, up 40% compared to March last year.

Construction Permits in Tbilisi

One of the most important signals is the reduction in future supply. In January–March 2026, the total area of issued construction permits fell by 31% year-on-year, reaching around 176,000 sq. m. In March, potential supply was estimated at 2,712 apartments, also significantly below last year’s level.

The slowdown in developer activity is partly linked to a high base in the previous period, but also reflects a more cautious approach to launching new projects. If current demand levels persist, this may create a risk of supply constraints in the medium term and support price levels.

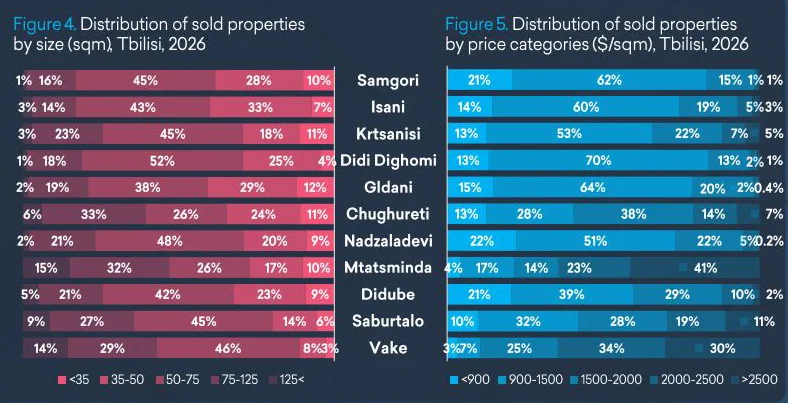

Prices and Market Dynamics by District

Tbilisi shows clear price disparities across districts. The highest levels remain in Vake at $2,400–2,500 per sq. m. Mtatsminda follows at $2,000–2,200, then Saburtalo at $1,700–1,800. In Isani and Didube, average prices range from $1,200–1,400, while in Samgori they are $1,000–1,100, and in Gldani around $900–1,000 per sq. m.

The strongest price growth was recorded in Isani (+10%), Mtatsminda and Nadzaladevi (both +9%). Vake saw around +7%, while Samgori and Didube grew by roughly +5%. Transaction dynamics also shifted: the fastest growth was seen in Krtsanisi (+84%), Saburtalo (+73%), and Mtatsminda (+61%). Significant increases were also recorded in Didube (+51%) and Gldani (+27%).

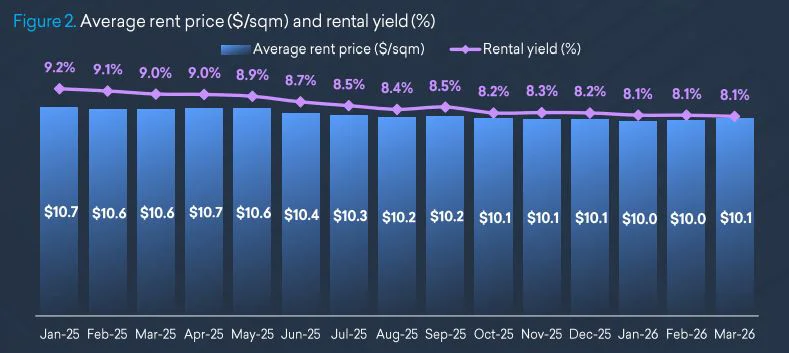

Rental Market and Yields in Tbilisi

The rental segment in 2026 shows a decline after previous growth. In Q1, average rent stood at around $10 per sq. m, down 6% year-on-year. In March, the figure was $10.1 per sq. m, down 5%.

Gross rental yield decreased to 8.1%, down about 1 percentage point year-on-year. It should be noted that this figure does not include maintenance costs; the real net yield is typically lower by a few percentage points (around 6%). With potential vacancy periods, it may be even lower.

Outlook: Transition Toward a More Balanced Market

Analysts at International Investment note that Tbilisi’s residential market is gradually moving away from sharp fluctuations toward a more stable development model. For end buyers, 2026 may represent a more comfortable entry point: pressure from overheated demand is easing, while secondary market supply is expanding, offering a wider range of options and more careful selection by location and quality.

At the same time, structural constraints on new supply remain in place. This could lead to renewed price growth in certain segments, particularly high-quality properties in well-established districts.

For investors, the picture is more mixed. Rental returns in Tbilisi are gradually declining, while the rental market is becoming more competitive. As a result, buy-to-let strategies require more precise calculations, including occupancy rates, seasonality, operating costs, and location-specific factors. In this context, hospitality investments in Georgia appear more resilient, supported by tourism inflows and continued infrastructure development.