The 'Nolan Effect': New 'Odyssey' Drives Wave of Tourists to Ancient Troy

The 'Nolan Effect': New 'Odyssey' Drives Wave of Tourists to Ancient Troy

New York Landlords Challenge Rent Freeze for One Million Apartments

New York Landlords Challenge Rent Freeze for One Million Apartments

Gold Holds Gains Before the Fed Decision

Gold Holds Gains Before the Fed Decision

Bitcoin Retreats Ahead of Federal Reserve Decision

Bitcoin Retreats Ahead of Federal Reserve Decision

Slovakia Keeps Housing Open to Foreign Buyers

Slovakia Keeps Housing Open to Foreign Buyers

EU Rules May Raise Housing Finance Costs

EU Rules May Raise Housing Finance Costs

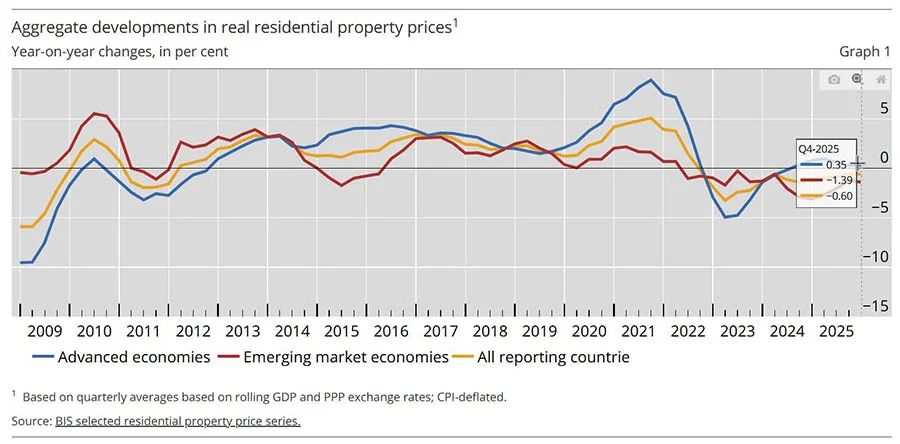

Global housing market ended 2025 with a decline in prices

The global residential real estate market continues to cool. At the same time, developed countries have broadly stabilised, while emerging economies continue to show a decline, especially in Asia, according to a study by the Bank for International Settlements (BIS).

Real and nominal house prices

In Q4 2025, global house prices adjusted for inflation fell by 0.6% compared to the same period in 2024. The pace was comparable to July–September and continued the trend of the past four years.

The BIS clarifies that this refers to real prices. At the same time, in nominal terms, housing worldwide is still becoming more expensive: in Q4 2025, growth amounted to 2.1%. Aggregated global indicators hide significant differences between countries.

The average value based on purchasing power parity (PPP) declined slightly, but median price growth remained close to 2%. Most countries still show positive dynamics. Price increases from 0% to 10% were recorded in 70% of developed economies and 60% of emerging ones. Large economies have a strong impact on global statistics, especially China, where a significant price decline continues, pulling aggregate indicators down.

Developed economies have stabilised

In developed countries, real house prices rose by only 0.4% in Q4 2025. The market as a whole has stabilised after a correction period observed since mid-2024. Especially strong growth was recorded in the euro area — 3%. In other European countries, the increase was 1.2%, while in developed economies outside Europe prices fell by 1.1%.

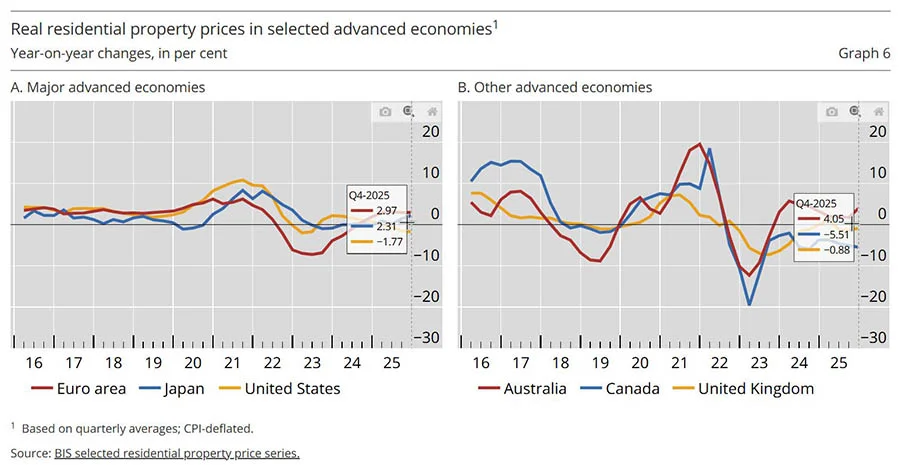

Among major markets, analysts highlight the United States, where real house prices fell by 2%. In Japan, by contrast, growth of 2% was recorded. The euro area is gradually recovering, while significant differences remain within the region. In Portugal, prices increased by 16%, in Spain by 10%, and in Germany and France dynamics were close to zero.

Among other developed economies, Australia maintained strong growth of around 4%. In the United Kingdom, the decline was about 1%. Canada continued to show one of the sharpest drops — minus 6%.

Emerging countries continue to decline

In emerging economies, real house prices fell by 1.4% year-on-year. The BIS records the fourth consecutive year of decline. The main pressure factor remains Asia, where prices fell by 3.2%. China (-6%) continued its long-term correction. In Indonesia (-2%), the market again moved into decline, while growth in Malaysia and the Philippines slowed noticeably.

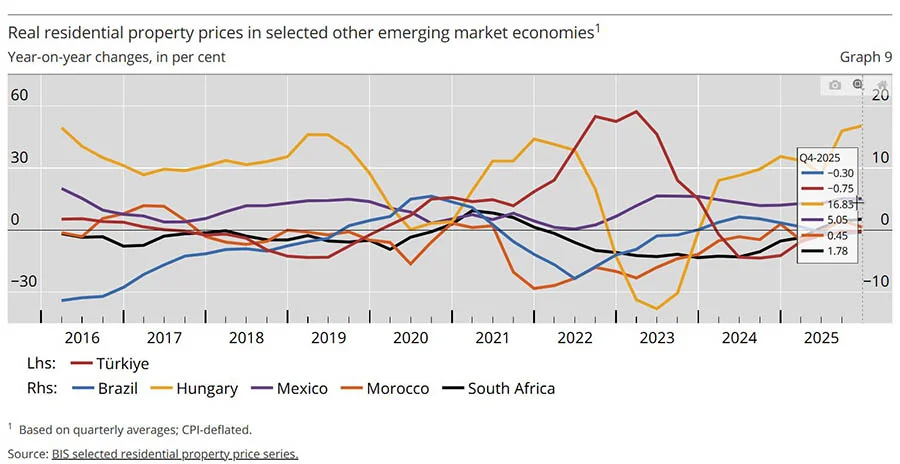

At the same time, some markets show signs of recovery. In Thailand, prices rose by 1%, while in India growth accelerated to 3%. In Latin America, prices continued to rise, mainly due to Mexico, where housing became 5% more expensive. In Brazil, the market remained stable. In emerging Europe, growth amounted to 4%, supported by a sharp jump in Hungary — 17%. In Turkey, prices fell by around 1%.

The group of African countries included in BIS statistics showed moderate growth of 1.4%. In South Africa, a slight recovery was recorded — plus 2%, while in Morocco there were virtually no changes.

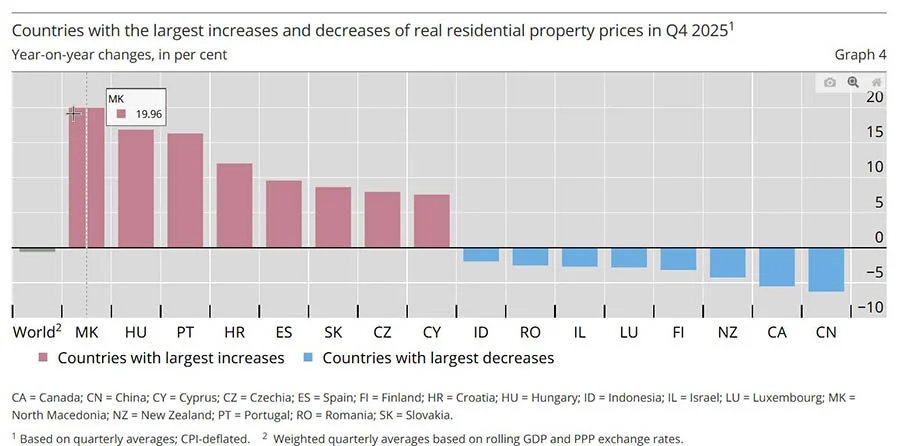

Growth leaders and laggards in real estate markets

The highest house price growth in Q4 2025 was recorded in North Macedonia — 20% in real terms. It was followed by Hungary (+17%) and Portugal (+16%). The sharpest declines were seen in China and Canada — both minus 6%, as well as in New Zealand — minus 4%.

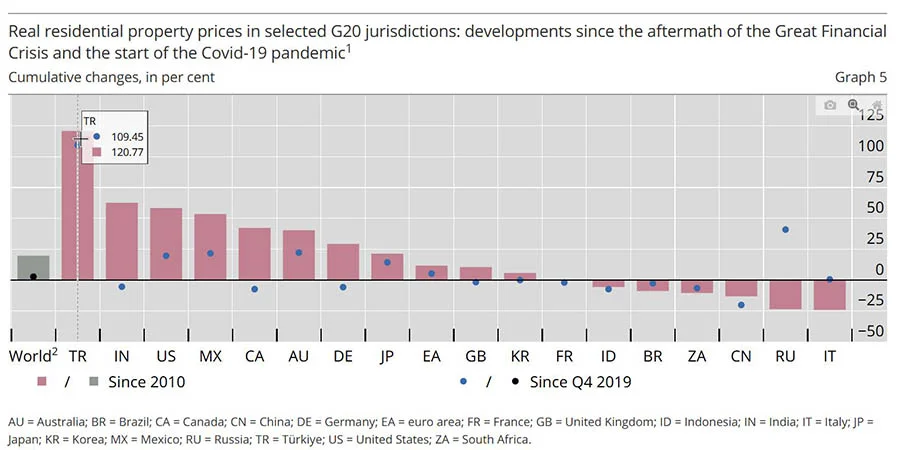

Since the end of 2019, i.e. since the start of the Covid-19 pandemic, global real house prices have increased by almost 3%. Among G20 countries, the absolute leader of growth was Turkey (+109%). Significant increases were also recorded in Australia and Mexico — +22% each. At the same time, China and Canada remain below pre-pandemic levels: declines of 20% and 7% respectively.

If comparing the current situation with the period after the global financial crisis of 2007–2009, global real house prices have increased by almost 20%. In many G20 countries, property prices are now significantly above post-crisis levels. In Turkey, prices have more than doubled, while in India, the United States and Mexico growth exceeded 50%. Several countries remain exceptions. In Italy, real house prices are still 24% below post-crisis levels. In China the gap is 13%, in South Africa 10%, in Brazil 9%, in Indonesia 6%.

Economic impact on the housing market

BIS data shows that the global housing market no longer follows a single trajectory. During the pandemic, many countries experienced simultaneous price growth due to cheap credit and stimulus measures. By the end of 2025, the situation has become more heterogeneous. Developed economies are gradually stabilising after a correction period, while emerging countries — especially in Asia — continue to face pressure.

Analysts at International Investment note that differences between national markets reflect the state of the economy and monetary policy of countries. High borrowing costs, inflationary pressure and slowing activity are restraining housing demand and limiting mortgage affordability in many regions. Countries where inflation is easing and conditions for monetary easing are emerging are gradually returning to growth, while in others the correction is prolonged. Global dynamics remain heavily dependent on the situation in the largest economies — above all China, where a prolonged downturn in the property sector continues to affect the global housing market.