Fed Split Revives Threat of Higher Rates

Fed Split Revives Threat of Higher Rates

Reviews Expose Argentina’s Tourism Weaknesses

Reviews Expose Argentina’s Tourism Weaknesses

Bank Indonesia Expands Support for Rupiah

Bank Indonesia Expands Support for Rupiah

Central Banks Return to Gold After Weak Start

Central Banks Return to Gold After Weak Start

Dubai Real Estate Market Slows Amid Middle East Conflict

Dubai Real Estate Market Slows Amid Middle East Conflict

Egypt launches digital visa-on-arrival system at Cairo International Airport

Egypt launches digital visa-on-arrival system at Cairo International Airport

Batumi Housing Market: Sales Growth and Risks of Oversupply

The Batumi housing market continues to show growth in both sales and prices, while increasingly reflecting the impact of the construction boom of recent years. A significant volume of unsold apartments remains in the primary market, and a large pipeline of new projects creates risks of oversupply, according to Galt & Taggart.

Apartment Sales in Batumi: Rising Figures

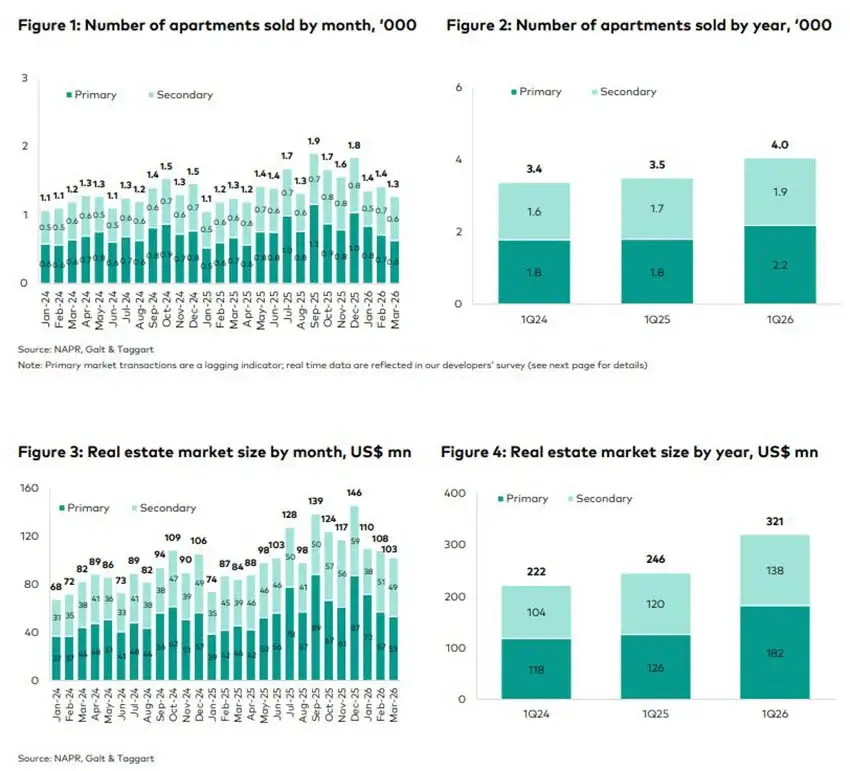

In the first quarter of 2026, 4,049 apartments were sold in Batumi. This is 15.8% higher than in the same period of 2025, according to the Public Registry of Georgia. Secondary market sales increased by 10.1%, while the primary market grew by 21.1%. At the same time, the authors of the study note that new-build statistics may be distorted due to delays in transaction registration.

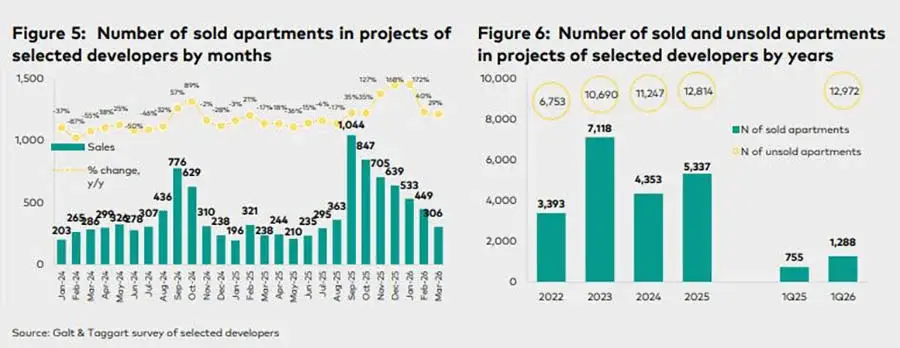

To assess current trends, the company also conducted a developer survey covering more than 30 active residential projects, representing about 40% of Batumi’s primary market. According to developers, the sales peak occurred in September 2025, when 1,044 apartments were sold in a single month. In 2026, monthly figures declined from 705 in January to 306 in March. Overall, in Q1 2026, participating developers sold 1,288 units versus 755 in the same period of 2025. At the same time, the volume of unsold apartments continues to grow and has reached nearly 13,000 units.

At the same time, the structure of supply is changing. In projects scheduled for completion in 2026, around 71% of apartments have already been sold, while in developments with completion dates in 2027–2029, the sales rate ranges between 53% and 56%.

Who Is Buying Property in Batumi

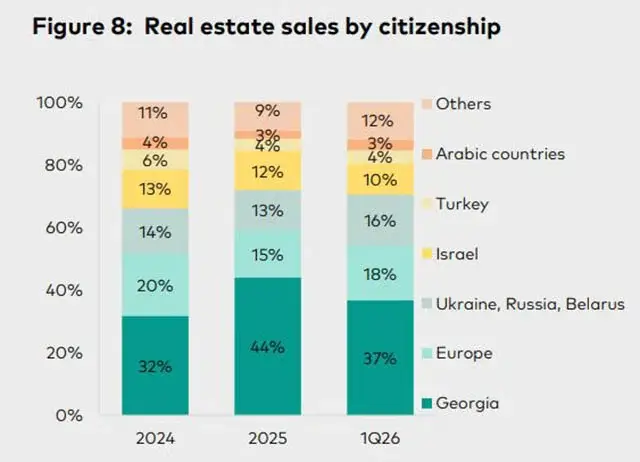

Georgian citizens remain the largest group of property buyers in Batumi, although their share has started to decline. Among developers participating in the Galt & Taggart survey, they accounted for 32% of sales in 2024, 44% in 2025, and 37% in Q1 2026. Domestic demand still accounts for more than one-third of total transactions.

Europe ranks second. Its share was 20% in 2024, fell to 15% in 2025, and is estimated at 18% in Q1 2026. European buyers remain the largest foreign group in Batumi’s housing market.

Buyers from Ukraine, Russia, and Belarus accounted for 14% of transactions in 2024, then 15% and 16% respectively. Israeli investor activity fluctuated from 13% to 12% and declined to 10% in early 2026. Israel remains one of the most significant foreign sources of demand.

Turkish buyers are also gradually reducing their presence, from 6% in 2024 to 4% in the first quarter of 2026. The share of buyers from Arab countries remains at 3–4%. Overall, the data reflects the international nature of demand in the Batumi real estate market.

Apartment Sales by District in Batumi

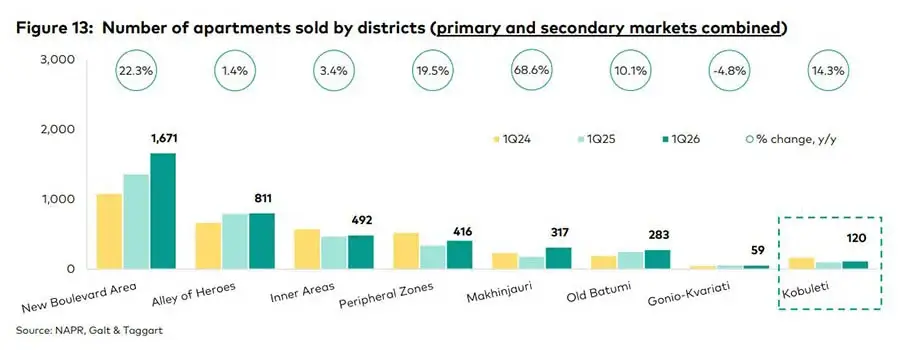

In Q1 2026, the New Boulevard district led in terms of apartment sales, with 1,671 transactions across both primary and secondary markets, up 22.3% year-on-year. The second position was held by the Alley of Heroes with 811 transactions, up just 1.4% compared to the previous year. Volumes remain high, but growth rates are clearly slowing.

In Makhinjauri, sales jumped by 68.6% to 317 apartments, while Kobuleti increased by 14.3% to 120 transactions. This may indicate growing buyer interest beyond central Batumi districts. Inner-city areas grew by 3.4% to 492 transactions, while peripheral locations declined by 19.5% to 416 units.

Apartment Prices in Batumi

Average Prices

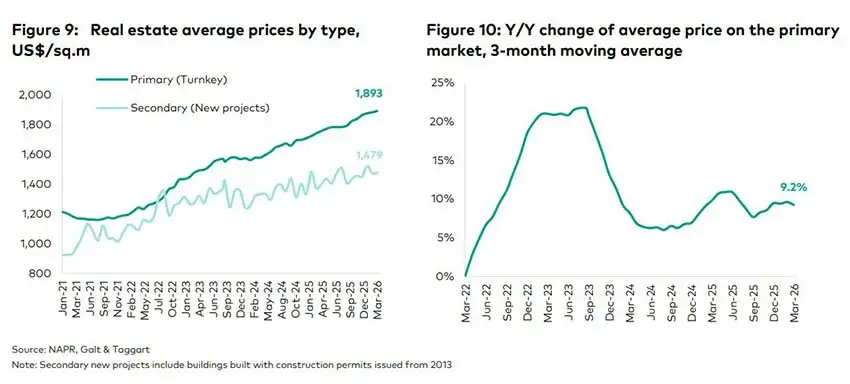

In March 2026, the average price of turnkey housing on the primary market reached $1,893 per square meter (+8.7%). On the secondary market, the average price stood at $1,479 per square meter (+7.8%).

Analysts highlight a significant price gap between the primary and secondary markets. Combined with a large pipeline of ongoing projects and gradually declining rental yields, this may limit the primary market’s ability to maintain current price growth rates for new developments.

Most Expensive Housing in Batumi

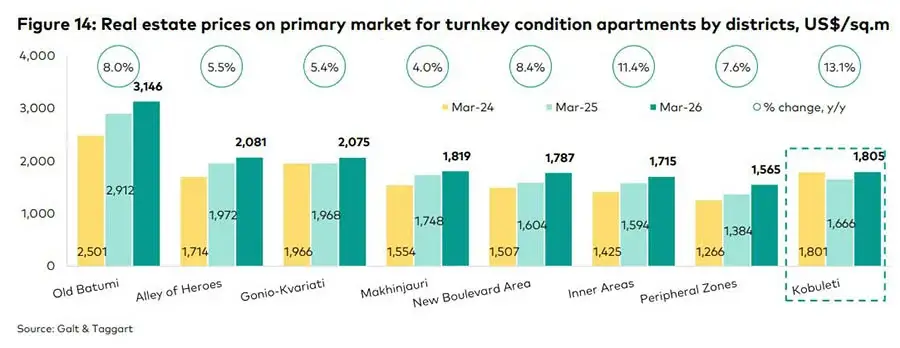

The highest-priced primary market properties are in Old Batumi, averaging $3,146 per square meter, up 8% year-on-year. The Alley of Heroes ranks second at $2,081 (+5.5%), closely followed by Gonio–Kvariati at $2,075 (+5.4%).

Fastest Price Growth

The fastest price growth was recorded in inner-city districts at +11.4% to $1,787. Kobuleti also showed double-digit growth (+13.1%) to $1,805. Despite leading in sales, New Boulevard remains cheaper on average than premium districts at $1,819 per square meter (+8.4%).

Most transactions remain concentrated in major urban districts, while both activity and price growth are increasingly shifting toward new and peripheral areas. Analysts also note significant price fluctuations across nearly all locations.

Rental Yield Declines in Batumi

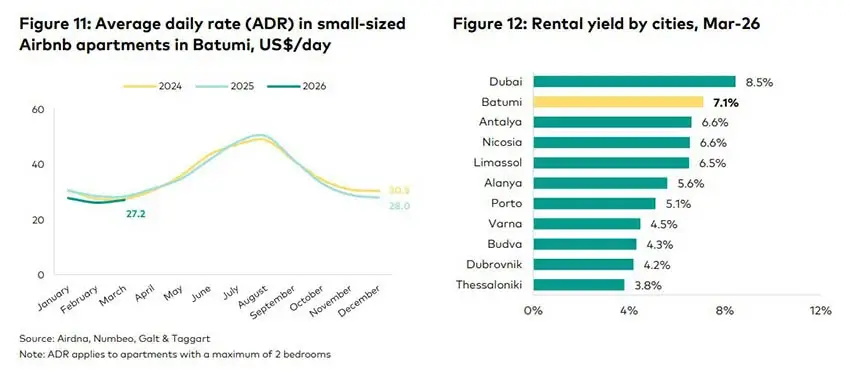

Average daily rental rates in Batumi fell by 7.3% in Q1 2026. At the same time, experts note that the rental market is highly dependent on the summer tourist season, which traditionally accounts for the bulk of demand.

Gross rental yield has declined from around 10% three years ago to 7.1%. According to Galt & Taggart, it may fall further to 5.1%, or in more conservative scenarios to 3.4%. While still high compared to similar cities, net returns after expenses are significantly lower.

Analysts at International Investment estimate that real rental returns are at the 2–3% level, and may drop to zero or negative during vacancy periods. As a result, the investment attractiveness of residential property in Batumi is gradually weakening.

Hotel Sector Investment

Hotels in Batumi significantly outperform apartments in terms of returns, reaching 10–17%. Even with higher per-square-meter costs, hotel room yields are approximately 4.8 times higher due to centralized operations. Management, marketing, bookings, reception, and maintenance are integrated into a single system, distributing costs across the entire asset.

Branded hotels in Batumi show stable occupancy growth: 2022 — 68.6%, 2023 — 70%, 2024 — 71%. An average nightly rate of around $286 confirms sector resilience even under conservative scenarios. However, the supply of high-quality hotels remains limited, mostly city hotels and a few international chains. New luxury and all-inclusive developments could strengthen the segment and improve income stability.

Conclusion

The number of transactions in Batumi’s housing market is rising, but primary market demand remains significantly below the 2022–2023 boom levels. At the same time, supply is increasing as construction continues at a high pace, intensifying pressure on the market.

Rental yields are already declining, and this trend continues. As unsold new-build stock accumulates, it is expected to increasingly influence price dynamics. Experts anticipate at least a slowdown in price growth, with more pronounced corrections in certain segments.

Against this backdrop, investment focus is gradually shifting. The most stable and attractive segment remains the hotel market in Batumi, particularly premium and luxury projects. This format is currently better adapted to tourism growth and provides more stable returns compared to residential assets.