Croatia Real Estate Market Grows Amid Supply Constraints

The Croatian real estate market in 2025 showed steady growth, which Colliers experts attribute to strong investor demand and limited availability of high-quality assets. The country’s economy was supported by declining interest rates, stable credit ratings, and low unemployment, which strengthened interest across key property segments.

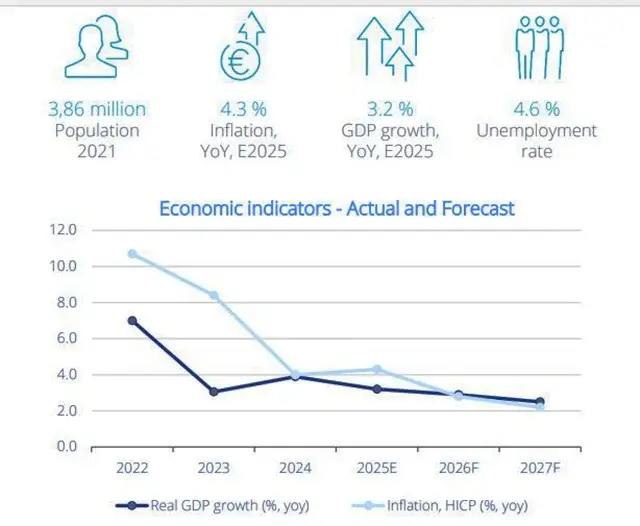

Croatia’s Economy: Positive Indicators

Croatia’s economy continued its stable growth trajectory in 2025. Real GDP is projected to increase by 3.2% in 2025, followed by a slowdown to 2.9% in 2026. Economic momentum is supported by lower interest rates and stable sovereign credit ratings.

The European Central Bank gradually reduced its key rates during 2025, with the MRO rate reaching 2.15% by June and remaining unchanged through year-end. Leading rating agencies reaffirmed Croatia’s sovereign credit: Moody’s at A3, S&P and Fitch at A-.

Inflation in 2025 is expected at 4.3%, driven by food and energy prices, while services inflation is easing. Unemployment fell to a record low of 4.6% and is expected to remain tight, with projections of 4.5% in 2026 and 4.6% in 2027, reflecting a constrained labor market.

Average net salary increased by 9.9% nominally and 6.6% in real terms, reaching €1,449.

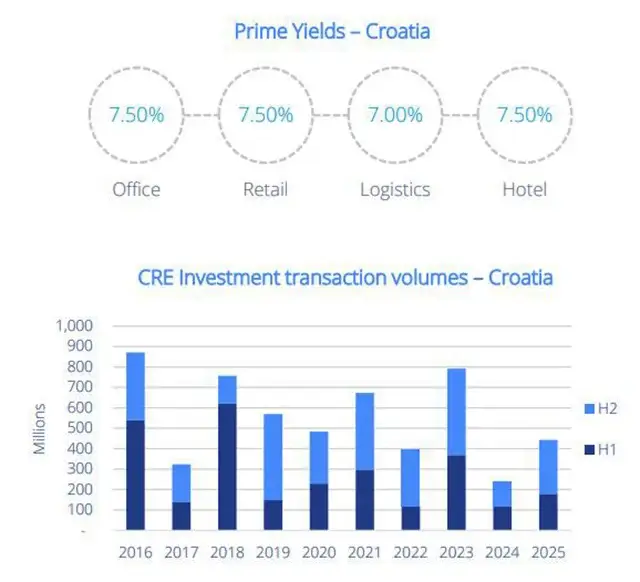

Investment Market in Croatia

Investor demand remains strong, particularly for stabilized income-generating assets with predictable cash flows. However, transaction volumes are constrained by the limited availability of institutional-grade product, making annual activity volatile and dependent on timing of large asset sales.

Investment activity is geographically concentrated, with Zagreb, Rijeka, and Split accounting for around 70% of total volumes. By sector, retail (retail) dominates with approximately 60% of total investment, driven mainly by large shopping center transactions, followed by the office sector.

Investors primarily focus on core and core+ assets with long WAULTs and strong tenant covenants. A key structural shift is the growing role of domestic capital, which accounts for about 70% of total transactions, compared to roughly 35% in 2020.

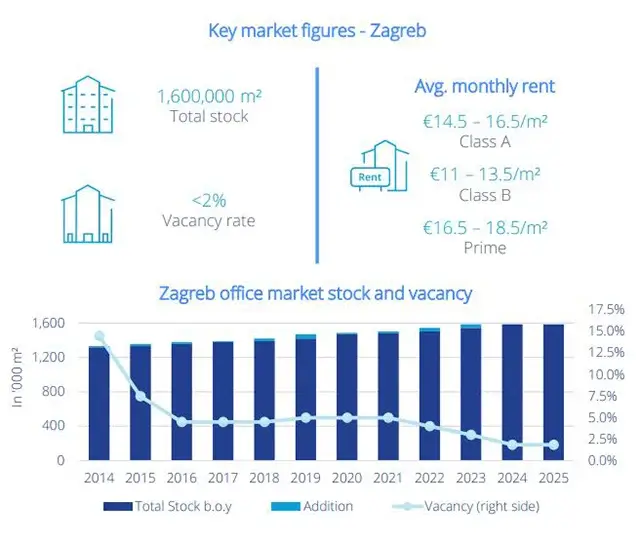

Office Market: Severe Supply Constraints in Zagreb

The Zagreb office market is characterized by structural undersupply of modern space. Vacancy rates have fallen below 2.5%, creating a strong landlord-driven market.

Demand remains stable and focused on high-quality Class A office space. Key drivers include business expansion, space optimization, and relocation from Class B and C buildings due to rising operational costs. Hybrid work models continue to reshape occupier requirements.

Subleasing activity has become more visible in recent years. Demand is concentrated in smaller units up to 300 sq. m, followed by 500–700 sq. m spaces, while strong interest remains for large-scale requirements above 2,000 sq. m from corporate and public sector tenants.

Rental growth is moderate but persistent, driven by limited supply and low vacancy. New construction remains limited, while the market structure is still dominated by older stock: Class B buildings account for the majority of supply, Class A represents around 45%, and modern assets younger than five years make up only about 3%.

Retail: Shift Toward Experience-Driven Formats

The retail segment in Croatia continues to transform toward experience-oriented formats. Entertainment, gastronomy, and service components are becoming increasingly important within shopping centers, including food courts and fresh food concepts.

Retail turnover has grown for 33 consecutive months, with total annual growth of 3.6% in 2025. Growth is supported by rising wages, employment, and stable tourism flows, while demand is gradually normalizing after the post-pandemic recovery period.

Retail parks play a key role in development activity, particularly in smaller and mid-sized cities. In 2025, 11 new retail parks were opened, adding more than 80,000 sq. m of space, while 19 additional projects under development or announced will contribute over 100,000 sq. m. Vacancy in prime shopping centers remains below 3%, supporting stable rental levels amid strong competition for high-quality space.

Industrial & Logistics: Expanding Supply Base

The logistics market in Croatia is in a phase of rapid expansion. Key hubs include Zagreb, Kukuljanovo near Rijeka, and Dugopolje near Split. Around 220,000 sq. m of new logistics space was delivered in 2025, with 111,500 sq. m under construction and an additional 615,000 sq. m announced.

Despite new deliveries, the market continues to face a structural shortage of modern Class A facilities. Vacancy remains at historically low levels due to strong absorption.

Demand is concentrated in modern, energy-efficient warehouses, particularly from 3PL providers and retail distributors. The most in-demand unit sizes range from 1,000 to 5,000 sq. m, with additional demand for large facilities above 20,000 sq. m.

Rental levels remain stable, with upward pressure in the premium segment due to limited availability and rising construction costs. The Rijeka Gateway project is further strengthening Rijeka’s position as a key logistics hub.

Hospitality: Focus on Quality and Investment Activity

Tourism continued to grow in 2025, with arrivals increasing by 2.3% and overnight stays by 1.3% year-on-year. The hotel sector recorded approximately 26.1 million overnight stays, up 2.5% compared to 2024. Seasonality remains pronounced, with July and August accounting for around 55% of total stays.

Key source markets include Germany (20%), Slovenia (10%), Austria, and Poland (7% each), while non-traditional and domestic markets are gaining share. Demand is shifting toward higher-quality accommodation. Modern, well-positioned hotels with strong amenities outperform the broader market.

Rising operating costs, particularly labor and energy, continue to pressure margins and limit pricing flexibility. Investor interest is increasing from both international and domestic capital, with a focus on value-add strategies, including repositioning, upgrading, and international operator entry.

Construction: Rising Activity and Cost Pressure

The construction sector in Croatia grew by approximately 7–9% year-on-year, driven mainly by infrastructure and tourism-related development, particularly in Zagreb.

However, cost pressures remain significant, including labor shortages, wage growth, material price volatility (especially steel and MEP systems), and stricter ESG requirements.

Industry participants increasingly focus on cost control, phased delivery, and value engineering. A 3–4% inflation buffer is recommended for budgeting through 2026.

Key risks include incomplete design documentation at tender stage, permitting delays, limited availability of Tier 1 contractors, and cost escalation during delivery. Projects with incomplete design inputs may experience cost increases of 10–20% and delays of 2–4 months.

Conclusion

International Investment analysts note that Croatia’s commercial real estate market remained highly active in 2025 across all major segments, including offices, retail, logistics, and hospitality. Developers continue to respond to demand by delivering modern, ESG-compliant assets.

At the same time, a key structural challenge is rising construction costs combined with limited supply in certain segments. Despite pricing pressure, strong underlying demand continues to support investment activity and development pipelines.

Overall, the market is shifting toward higher-quality, more modern assets. However, the balance between supply and demand remains tight, particularly in the institutional investment segment.