The global economy is slowing due to inflation and the energy crisis

Bloomberg

Global inflationary pressure and the energy crisis have persisted for the third month amid the war with Iran. Industrial activity has slowed or contracted in most countries, with the exception of the United Kingdom and the United States. Long-term government bond yields in the G7 countries have reached their highest level in over 20 years, Bloomberg reports.

Global manufacturing is losing momentum

Global industrial activity continued to weaken in May: S&P Global business activity indices either declined further or moved into contraction territory in almost all major economies. The only exceptions were the United Kingdom and the United States, where indicators remained above the threshold of decline.

The most pronounced deterioration was recorded in the euro area. In Germany and France, manufacturing indicators fell into contraction territory, with France experiencing a particularly sharp and unexpected decline. Overall, the region is transitioning into a phase of industrial slowdown.

A similar pattern is observed in other parts of the world: purchasing managers’ surveys show that businesses in Australia and several Asian economies are also facing worsening operating conditions and weaker demand. As a result, the slowdown is broad-based and affects several key centers of the global economy.

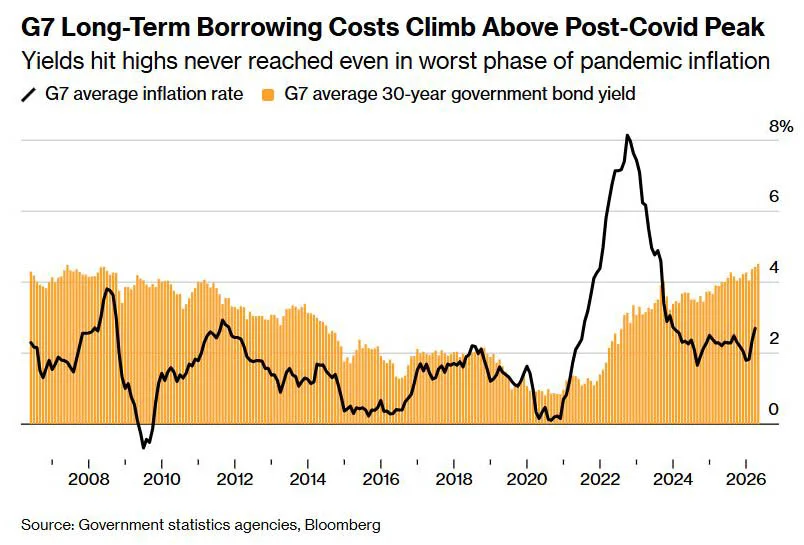

G7 government bond yields hit 20-year highs

Financial markets are increasingly reacting to a prolonged inflationary impulse linked to the energy crisis. Yields on long-term government bonds across the G7 rose this week to their highest levels in two decades.

This refers to a market exceeding $50 trillion, traditionally considered one of the most stable segments of the global financial system. The rise in yields reflects growing investor sentiment that the current inflation surge may not be a one-off event, but rather a sustained trend driven by repeated energy shocks in the 2020s. Pressure is also spreading across other segments of global markets, where borrowing costs are gradually being repriced higher.

Central bank decisions

Monetary policy is increasingly diverging across countries. Some central banks continue tightening in response to persistent inflationary pressure, while others opt to keep rates unchanged.

Among countries that raised rates were Indonesia and Mauritius, where policy moves were more aggressive than expected by markets. Meanwhile, central banks in Egypt, Nigeria, Ghana, Jamaica, and Paraguay kept key rates unchanged, adopting a wait-and-see approach.

In Iceland, where inflation has remained persistently elevated for an extended period, the central bank raised borrowing costs for the second time, continuing its tightening cycle after the onset of the energy shock. As of March, inflation in the country had remained above 5% for four consecutive months.

Rice market reacts to weak harvest forecasts

Global food markets are seeing increasing price pressure: rice prices have risen to their highest level in more than a year. The increase is driven by deteriorating harvest expectations and higher production costs, including fertilizer prices.

An additional factor is climate conditions associated with El Niño, which are increasing uncertainty in the agricultural sector. Against this backdrop, market participants are increasingly pricing in the risk of reduced supply.

According to the US Department of Agriculture, global rice production in the 2026–2027 season could decline for the first time in 11 years, raising concerns about the stability of the global food market.

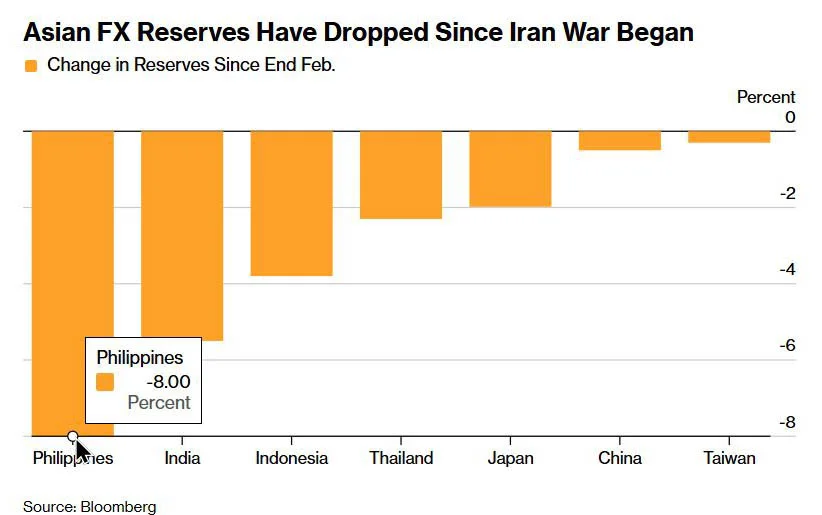

Financial imbalances intensify in Asia

In Japan, credit growth is now outpacing deposit growth, a situation previously considered unlikely. The country is experiencing a sharp increase in borrowing driven by rising business investment and corporate buyouts.

In Indonesia, India, and the Philippines, signs of financial stress are also intensifying. These economies are facing capital outflows and weakening national currencies. Central banks are being forced to tighten monetary policy despite deteriorating economic conditions. Additional pressure is coming from global bond markets, where volatility is increasing.

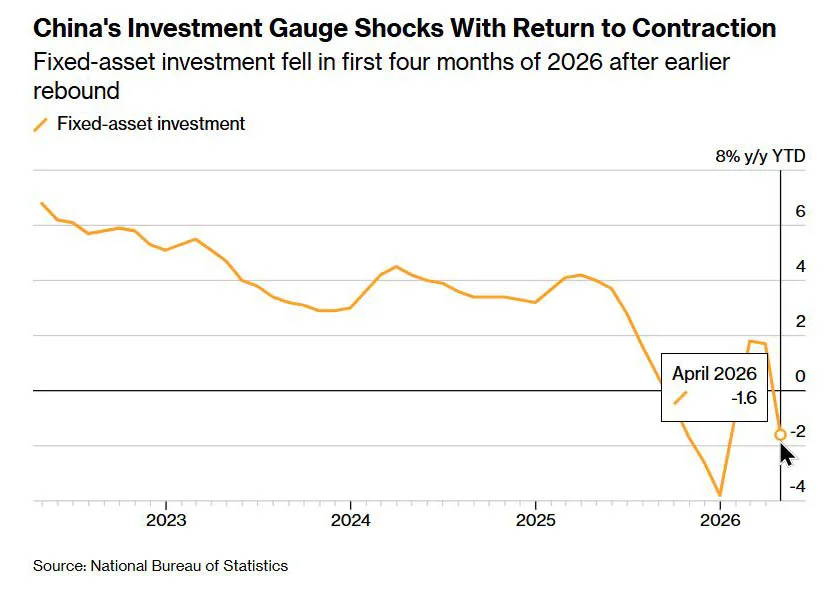

In China, investment continues to decline, raising questions about the authorities’ reluctance to introduce stronger stimulus measures. The global energy crisis is affecting production and consumption worldwide. Official data indicate that earlier export growth is no longer offsetting weakening domestic demand, resulting in a loss of economic momentum across several key components.

European economy

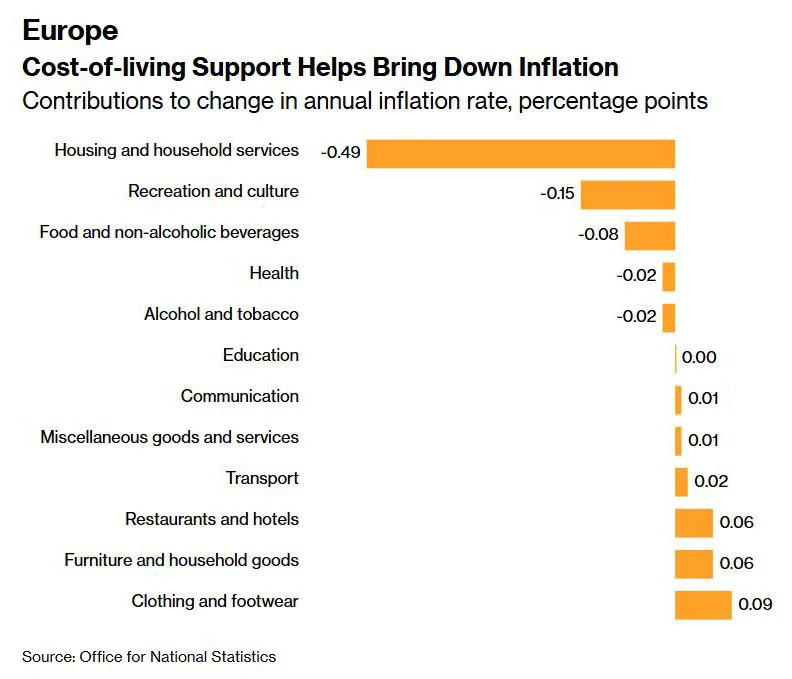

In the United Kingdom, inflation has slowed to its lowest level in over a year. The consumer price index rose by 3.3% in March and by 2.8% in April compared to the same periods in 2025. The decline is attributed to a favorable base effect and government support measures, including energy bill subsidies. Markets have begun to price in fewer rate hikes from the Bank of England, although some economists expect inflationary pressures to return later.

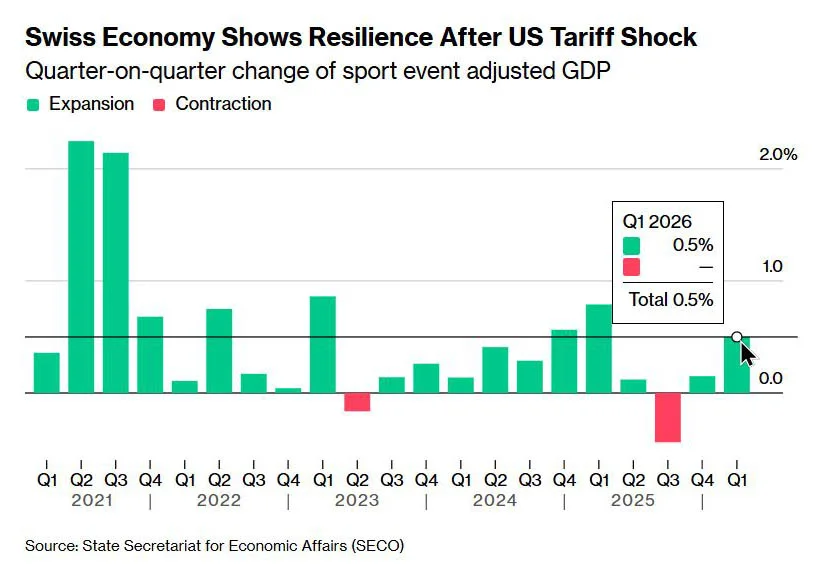

In Switzerland, the economy grew more strongly than expected. In the first quarter, GDP increased by 0.5% compared to the previous three months, according to preliminary estimates from the State Secretariat for Economic Affairs (SECO). The economy withstood the surge in energy prices and the strengthening of the franc that accompanied the onset of the Middle East conflict.

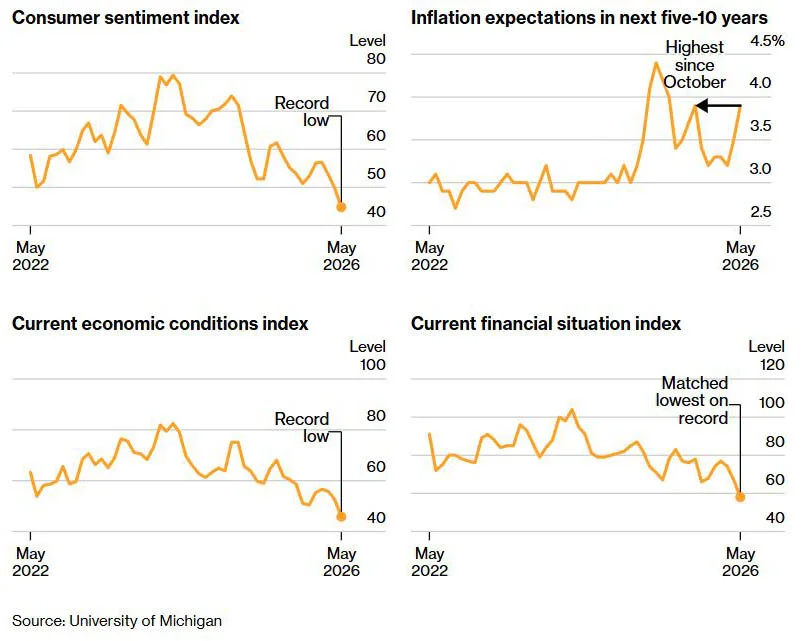

United States: record decline in sentiment

Consumer sentiment in the United States fell in May to a record low. Long-term inflation expectations deteriorated, driven by rising gasoline prices and ongoing uncertainty.

Additional pressure is visible in the housing sector. In April, the number of new housing starts declined, with single-family home construction falling at the sharpest pace in nearly a year. Building permits for single-family homes dropped to an eight-month low, indicating caution among developers amid high mortgage rates.

Conclusion

Analysts at International Investment note that the global economy is no longer moving in sync: industry, financial markets, and consumer demand are responding differently to current shocks, increasing divergence between regions and sectors. This reduces the predictability of overall dynamics and complicates the formation of a unified monetary response.

Higher bond yields and central bank decisions are reinforcing tighter financial conditions, which are already beginning to affect investment and credit activity. At the same time, dependence on external capital flows and price dynamics is increasing for individual economies.

As a result, an environment is forming in which localized improvements do not translate into sustained global growth, while external shocks are transmitted more rapidly across markets and sectors. Outlook depends on developments in the Middle East, where renewed tensions continue, including US strikes and sharp statements from Iran.