Fed Split Revives Threat of Higher Rates

Fed Split Revives Threat of Higher Rates

Reviews Expose Argentina’s Tourism Weaknesses

Reviews Expose Argentina’s Tourism Weaknesses

Bank Indonesia Expands Support for Rupiah

Bank Indonesia Expands Support for Rupiah

Central Banks Return to Gold After Weak Start

Central Banks Return to Gold After Weak Start

Dubai Real Estate Market Slows Amid Middle East Conflict

Dubai Real Estate Market Slows Amid Middle East Conflict

Egypt launches digital visa-on-arrival system at Cairo International Airport

Egypt launches digital visa-on-arrival system at Cairo International Airport

European Real Estate Recovery Gains Pace in 2026

The European real estate market is entering 2026 with renewed momentum after a politically turbulent and cautious 2025. Resilient economic growth, inflation close to target and improving investor sentiment are creating a more constructive backdrop for property markets across the region. Analysts expect income-driven returns to strengthen while selected sectors benefit from limited supply and recovering demand.

European economic outlook: growth stabilises

Recent industrial production and retail sales data indicate that the eurozone closed 2025 on firmer footing than previously expected. Despite slightly weaker Purchasing Managers’ Indices in December, underlying momentum has held up, supported by moderate fiscal easing.

Eurozone GDP is forecast to expand by 1.2% in 2026 and accelerate to 1.5% in 2027. Inflation reached the European Central Bank’s 2% target in December and is expected to dip temporarily below target in early 2026 before returning to around 2% by year-end.

The ECB deposit rate is projected to remain at 2% through 2026, with any potential rate hike likely postponed until 2027. Stable monetary conditions are providing a clearer framework for real estate investors.

European real estate market overview

After sentiment was weighed down by political uncertainty in 2025, European property markets are showing signs of stabilisation. The MSCI Pan-European Index delivered a 6.5% return in local currency terms in the third quarter of 2025, matching the previous quarter’s performance.

European REITs remain at discounts to net asset value, yet the FTSE EPRA NAREIT Europe Index rose 8% over the year to 19 January 2026, signalling improved investor expectations.

The INREV Confidence Indicator climbed to 59.4 in December 2025, close to its previous peak. The share of non-listed real estate investors planning to increase allocations rose to 38%, up from 18% a year earlier. Total investment volumes reached approximately €200 billion in 2025, still below the long-term average but indicative of gradual capital market recovery.

Office markets: supply constraints support prime assets

European office markets remain polarised. Vacancy rates rose to 15.1% in September 2025, yet new supply has declined steadily for five years and is now at its lowest level since 2016. New completions are expected to account for only 0.6% of total stock in 2026 and 2027, half the long-term average.

Prime rental growth remains strong at 5.3%, supported by limited high-quality space in core central business districts. Investors are increasingly focusing on resilient, well-located assets, including selected grade B+ offices in supply-constrained markets.

Industrial and logistics: structural demand intact

The logistics sector is stabilising after a period of occupier caution. Vacancy rates declined from 6.4% to 5.9% by September 2025, while rents increased by 4.8% year-on-year.

Long-term demand drivers remain compelling, including e-commerce expansion, nearshoring and supply chain diversification. Europe’s push for greater strategic autonomy in pharmaceuticals, green technologies and defence is expected to generate additional demand for industrial and distribution facilities.

Retail property: income resilience returns

Retail has been among the strongest-performing sectors over the past year. Investment volumes reached €23 billion in 2025, accounting for 16% of total market activity. European shopping centres delivered returns of 8.8% year-on-year to September 2025, closely aligned with retail warehouses at 9.2%.

Solid household balance sheets and real wage growth of 2.6% in December 2025 are supporting domestic consumption. Limited supply and asset repositioning efforts continue to underpin rental growth and income stability.

Residential sector: strongest fundamentals

The living sector remains underpinned by powerful structural demand and constrained supply. Vacancy rates declined to 2.3% in September 2025, the lowest among major property sectors.

Residential rents rose 5.7% year-on-year to September 2025, outperforming other sectors. Approximately 24% of total investment capital was allocated to residential assets, matching office investments. Policy reforms in Sweden, effective from January 2026, aim to encourage new development and investment activity.

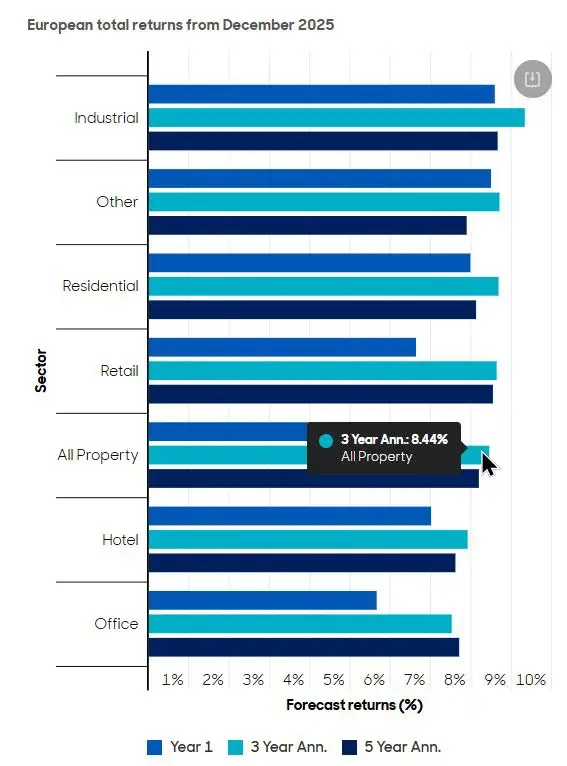

Performance outlook and key risks

Total property returns stood at 6.5% as of September 2025. Returns are projected to rise to 7.1% over the next year, with three- and five-year annualised forecasts at 8.4% and 8.2%, respectively. Income growth is expected to be the primary driver of near-term performance.

Key risks include geopolitical tensions, potential upward pressure on sovereign bond yields and economic slowdown. However, constrained supply and stable rental income provide a degree of insulation against macroeconomic volatility.

As reported by experts at International Investment, the European real estate market in the first quarter of 2026 is transitioning from stabilisation to moderate recovery. With inflation under control and growth holding steady, residential, logistics and selected core office assets are positioned to anchor diversified investment strategies in the years ahead.