Middle East conflict increases pressure on Gulf hotels

The hotel market in Gulf countries has come under pressure due to the Middle East conflict, which has hit air connectivity and tourism demand. Investors have become more cautious, are revising project timelines and tightening liquidity controls, while still maintaining interest in the sector, according to consulting firm HVS, which surveyed owners and investors with a combined portfolio of around 160,000 hotel rooms in the region.

Conflict hits aviation and tourism demand

Experts describe the US–Iran conflict as one of the most significant geopolitical shocks for the Gulf hotel sector since the COVID-19 pandemic. The main impact has been on air travel, while traveller confidence in safety has also weakened.

The war began during one of the most profitable periods for the regional hotel industry, which runs from March to May. During this time, hotels traditionally generate strong revenues due to religious tourism, business travel, MICE activity (meetings, incentives, conferences and exhibitions), spring leisure travel, and international visitor flows.

According to the World Travel & Tourism Council (WTTC), the region was losing around $600 million per day at the height of the crisis due to reduced tourist spending. After the announcement of a ceasefire and easing of airspace restrictions, the situation began to gradually stabilise, although investment sentiment remains cautious.

Who participated in the survey

The study included hotel owners, developers, investors, and companies operating in hotel real estate. The largest share of respondents came from Saudi Arabia — 42%, followed by the United Arab Emirates with 34%. The remaining responses came from Kuwait, Bahrain, Oman, and Qatar.

Among participants, 38% were hotel investment companies, 30% were real estate developers, and another 23% were private investors. The study primarily reflects the perspective of asset owners and capital providers rather than hotel operators.

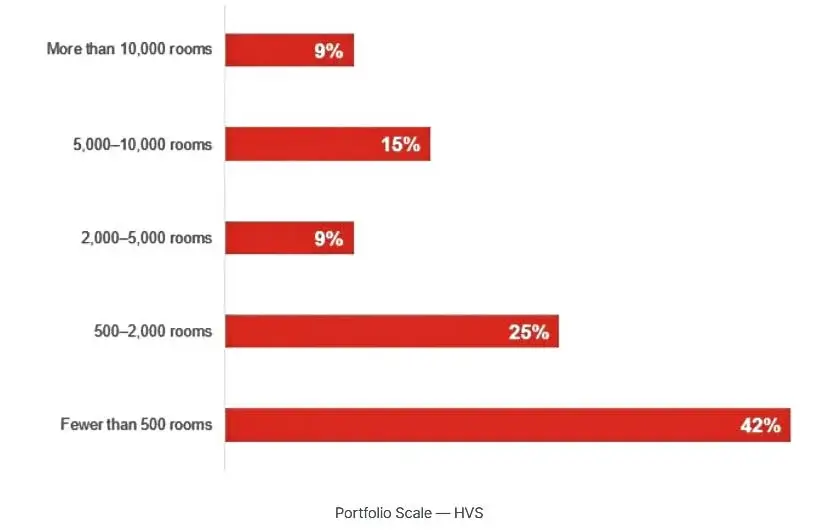

According to HVS, respondents collectively represent around 160,000 branded hotel rooms across GCC countries. Small and mid-sized portfolios dominate numerically, although the sample also includes large institutional players capable of withstanding short-term volatility.

Investors are more cautious, but have not left the market

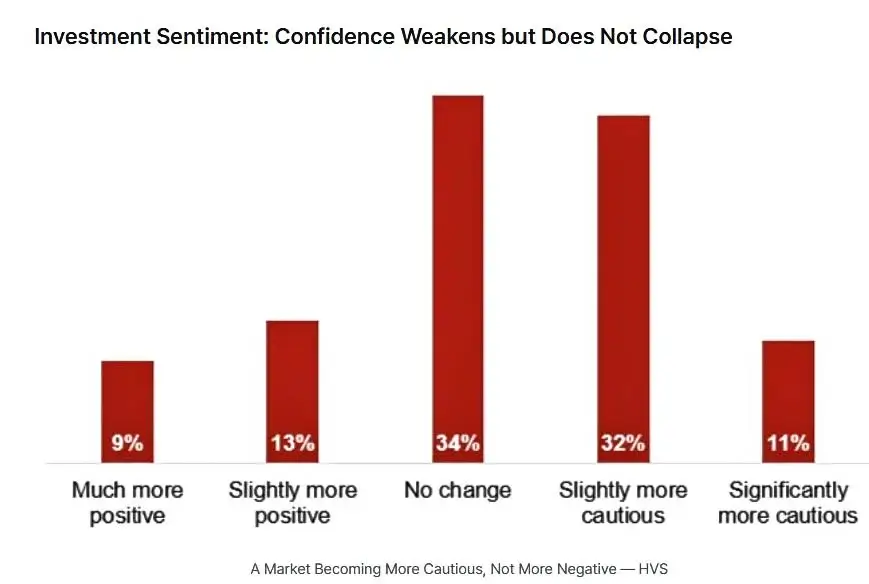

The conflict has noticeably shifted investment sentiment. Around 43% of respondents reported becoming more cautious after the conflict began, while 11% described themselves as “significantly more cautious”. Another 34% saw no major changes, and 22% reported an even more positive outlook.

The study highlights an important difference compared to the COVID-19 period. Investors view the current crisis as temporary, geographically limited, and mainly related to transport disruptions rather than a systemic collapse in demand.

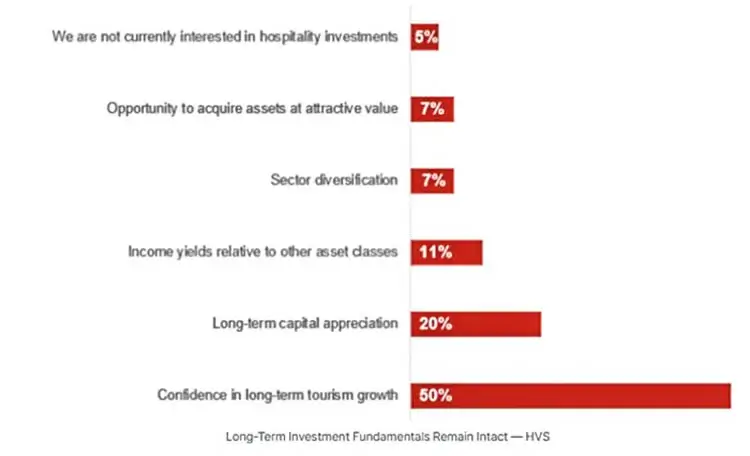

Short-term uncertainty has increased, while 83% of respondents still view hotel investment prospects in the Gulf as positive or neutral. Only 17% express a negative outlook.

Hala Matar Choufany, President of HVS for the Middle East, Africa and South Asia, notes that the market is not withdrawing from hotel investment, but is instead reassessing risks, liquidity, project timelines, and capital allocation in a more geopolitically uncertain environment.

Hotels driven by domestic and religious demand prove more resilient

The conflict has widened the gap between different types of hotel assets. Hotels focused on domestic tourism, religious travel, and staycations have proven more resilient. Hotels dependent on international travellers, air connectivity, corporate trips, and business tourism have been hit the hardest.

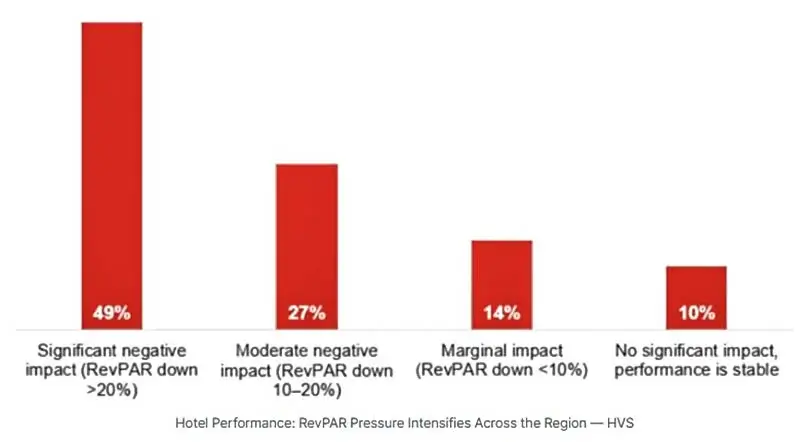

Nearly 76% of participants reported a noticeable or significant decline in RevPAR (revenue per available room). Almost half of respondents recorded a drop of more than 20%. In the hotel industry, such a decline typically puts serious pressure on profitability and EBITDA.

Experts note that recovery in occupancy alone does not guarantee a return to previous profitability. Financial performance is also influenced by average daily rate (ADR), inflation in operating costs, utility expenses, and rising supply chain costs.

Delays in new developments and investment decisions

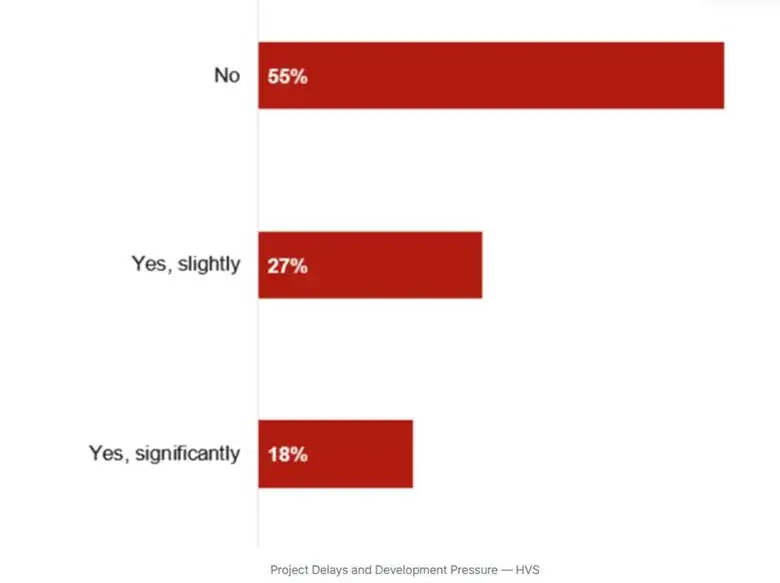

The conflict is already affecting hotel project timelines. Around 45% of respondents reported delays in investment and development decisions, with 18% noting significant postponements. The most resilient projects are those with strong ownership structures, stable domestic demand, and support from national tourism strategies.

The main short-term strategy among investors has been capital preservation. Asset owners prefer to hold existing hotels, reduce or defer capital expenditure, slow down new developments, and renegotiate agreements with operators and brands.

The market has not stopped entirely. Around 41% of participants still plan to build or acquire hotel assets within the next 12 months. Intention to sell assets remains very limited.

No mass hotel closures

Unlike during the pandemic, no widespread hotel closures have been recorded. Around 68% of respondents said properties continue operating despite weaker performance. Another 27% reported stable operations.

About 57% of participants believe their hotel assets will be able to meet key financial obligations for at least six months if current conditions persist.

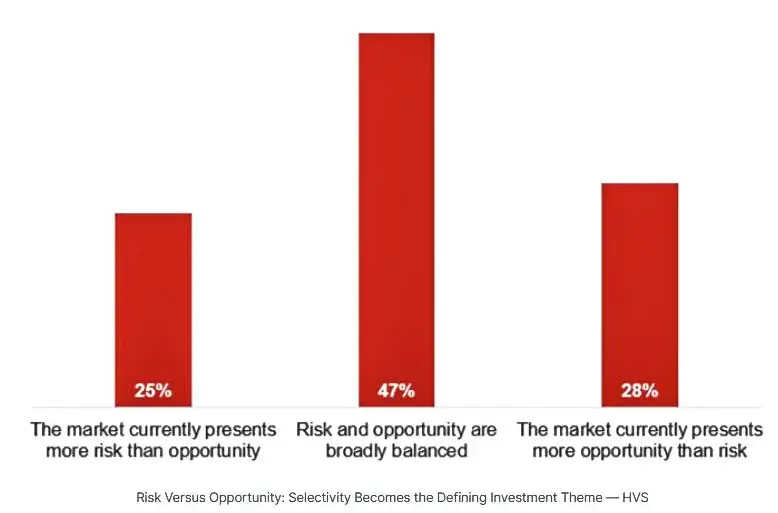

Hotel asset values are already under pressure, although the scale of correction remains uncertain. Most respondents expect a decline of less than 10% or consider the market too uncertain for precise valuation.

Risks for the Gulf hotel market

The most serious risk for the Gulf hotel industry, according to investors, is disruption to air connectivity. HVS emphasises that aviation is a critical piece of infrastructure for the region, enabling tourism flows, business mobility, and hotel occupancy.

Additional factors highlighted include weakening tourism and corporate demand, the possibility of further escalation of the conflict, and rising construction and operating costs.

HVS believes the current situation reflects not a loss of confidence in the sector, but a reassessment of risk, investment timing, and cost of capital. The market is entering a phase of more cautious and disciplined investment, with a focus on asset resilience and selective expansion.

Conclusion

Analysts at International Investment emphasise that security remains the key factor for the tourism industry in the Gulf states. The conflict has not yet been resolved, negotiations show limited progress, and the risk of further escalation remains, potentially involving not only Iran, Israel, and the United States, but also other countries in the region. Events in March have already demonstrated how quickly the situation can affect transport flows and tourism activity.

If the geopolitical situation stabilises, the recovery of air connectivity will become the main driver of renewed demand for hotel services and gradual improvement in the investment climate. At the same time, the sector has demonstrated resilience even under military tension, maintaining operational activity and a baseline revenue stream.

Investor interest in the sector remains intact. Hotel real estate continues to be one of the key investment areas in the region and globally. However, many investors have redirected activity toward safer locations, including Georgia in particular. The country has not been affected by armed conflicts — its economy is developing steadily, tourism is growing, and new projects are being implemented, including developments by major UAE-based developers.