Fed Split Revives Threat of Higher Rates

Fed Split Revives Threat of Higher Rates

Reviews Expose Argentina’s Tourism Weaknesses

Reviews Expose Argentina’s Tourism Weaknesses

Bank Indonesia Expands Support for Rupiah

Bank Indonesia Expands Support for Rupiah

Central Banks Return to Gold After Weak Start

Central Banks Return to Gold After Weak Start

Dubai Real Estate Market Slows Amid Middle East Conflict

Dubai Real Estate Market Slows Amid Middle East Conflict

Egypt launches digital visa-on-arrival system at Cairo International Airport

Egypt launches digital visa-on-arrival system at Cairo International Airport

Cyprus real estate market is changing its demand structure — PwC

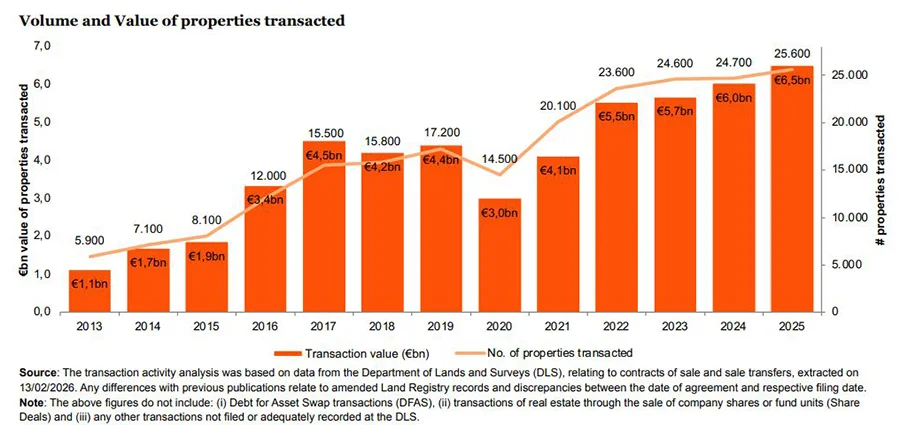

In 2025, a total of 25,600 real estate transactions were recorded in Cyprus, 4% higher than in 2024. The total transaction value increased by 8% to €6.5 billion, according to PwC analysts. A key trend was the gradual shift in demand structure across regions. Buyer activity is increasingly moving beyond traditional centres, while former leading markets are showing more moderate dynamics.

Residential segment: the backbone of the Cyprus real estate market

In 2025, the residential real estate market in Cyprus continued to grow, reaching approximately €4.5 billion, about 10% higher than in 2024. A total of around 15,900 properties were sold, including about 11,000 apartments and 4,900 houses, representing a 7% annual increase.

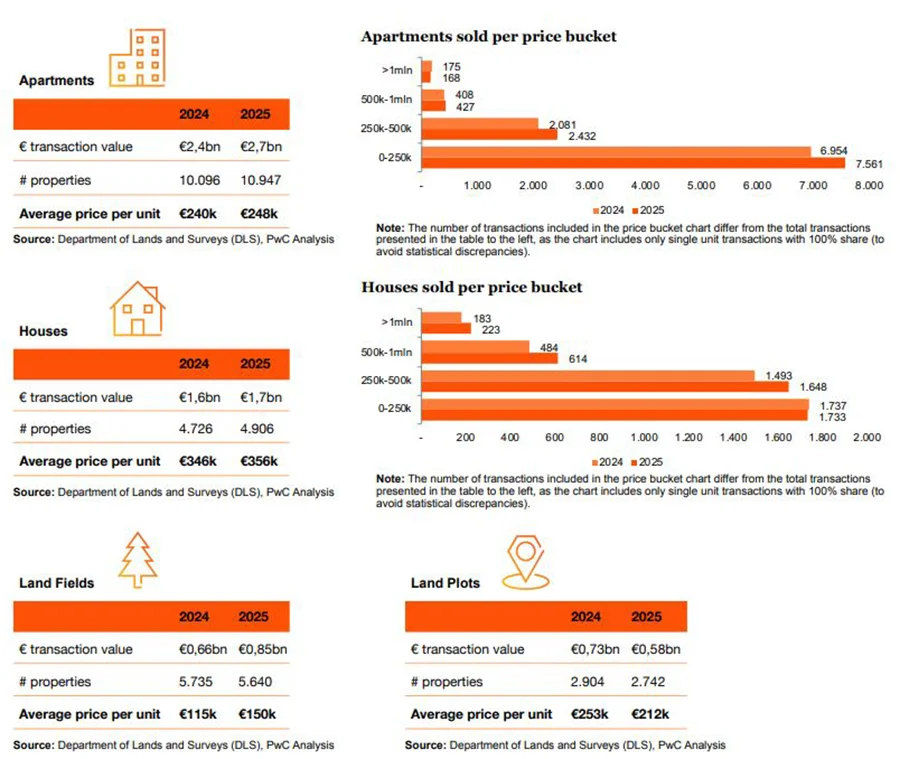

The residential segment accounted for the largest share of market activity, representing about 69% of total transaction value in the real estate sector. Apartments accounted for 42% of transaction value, houses for 27%, while the share of commercial property and land assets remained significantly lower.

An additional indicator of stable growth was the increase in average monthly transaction value, which rose from €503 million to €543 million. This reflects a gradual strengthening of the market throughout the year, while residential property continued to dominate demand.

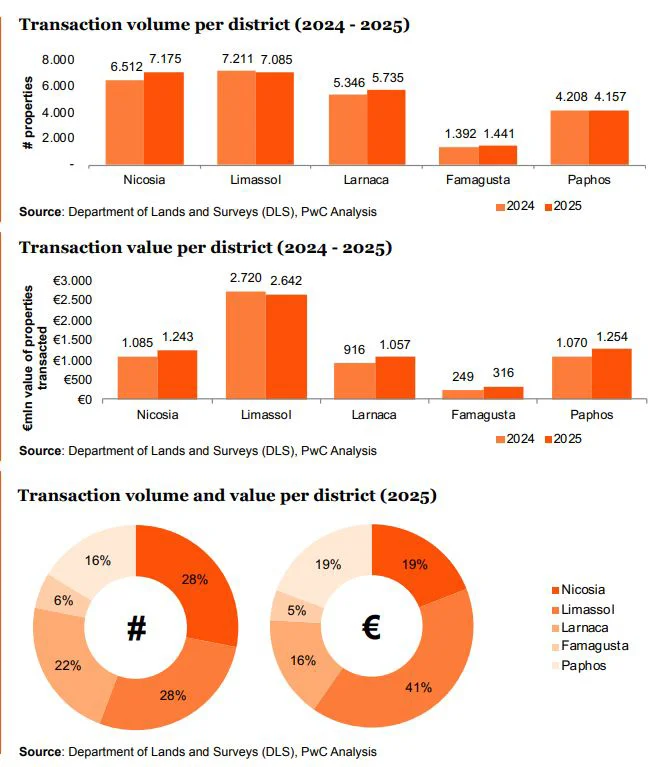

Nicosia: leader in transaction volume and growth

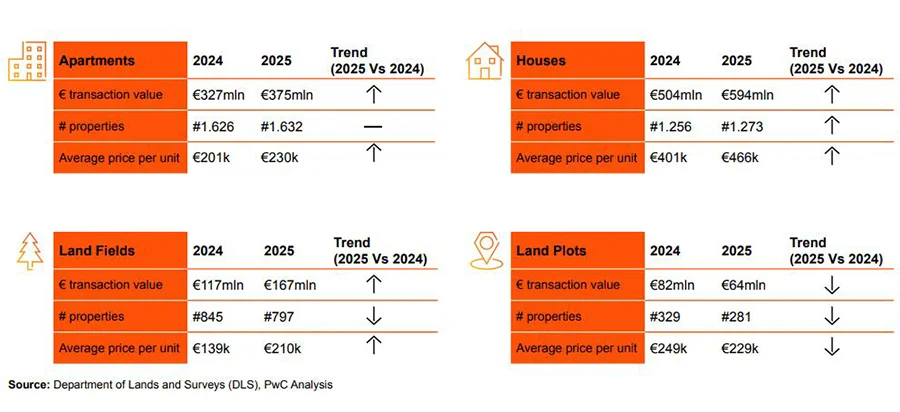

Real estate transactions in Nicosia increased by 10% in 2025, from 6,512 to 7,211, accounting for 28% of total transactions in Cyprus. Transaction value rose by 15% to €1.24 billion, reflecting stronger market activity amid overall expansion.

Apartments were the main driver of growth. The number of transactions increased from 2,541 to 2,995, while total value rose from €448 million to €529 million, with average prices remaining stable at around €176–177k.

House sales increased from 901 to 1,097, with total value rising from €208 million to €268 million. Average prices increased from €231k to €244k, reflecting stronger demand in the higher-end residential segment.

The land market showed a mixed picture. In land fields, the number of transactions remained almost unchanged (1,640 vs 1,644), while value increased from €102 million to €114 million. In the land plots segment, transactions declined from 988 to 977, while total value rose from €174 million to €181 million.

Limassol: decline in property sales performance

Limassol recorded 7,085 transactions, a 2% decline. Total transaction value also decreased from €2.72 billion to €2.64 billion (–3%). Despite this, the market share remains high, at 28% by volume and 41% by value.

Apartments remained the dominant segment. Sales increased from 2,928 to 3,081, while total value remained broadly stable at around €1.2 billion. Average prices rose from €395,000 to €403,000.

The residential house segment showed the opposite trend: transactions fell from 1,243 to 1,124, while total value declined from €566 million to €465 million. Average prices also decreased from €455,000 to €414,000, indicating weaker activity in the higher-end private segment.

In land fields, transactions declined from 1,872 to 1,777, while value increased from €296 million to €365 million, with average prices rising from €158k to €206k, reflecting land price inflation amid lower turnover. In the land plots segment, transactions fell from 828 to 723, and value dropped from €369 million to €216 million. Average transaction value also declined from €446k to €298k.

Larnaca: steady expansion of the real estate market

Larnaca recorded a 7% increase in activity, reaching 5,735 property transactions. Total value rose by 15% to €1.06 billion. The region strengthened its position, accounting for 22% of total market activity.

Apartment transactions increased from 2,548 to 2,808, while value rose from €423 million to €500 million. Average prices increased from €166,000 to €178,000, reflecting steady price growth alongside rising demand.

House sales increased from 891 to 951, with value rising from €223 million to €256 million. Average prices increased from €251k to €269k.

In land fields, transactions rose from 1,024 to 1,068, with total value increasing from €117 million to €141 million. In land plots, transactions declined slightly from 647 to 626, while value remained broadly stable at €100 million and €101 million. Average transaction value increased from €154k to €161k.

Paphos and Famagusta: trends in apartments and land

In Paphos, 4,157 transactions were recorded, 1% lower than in 2024. However, total value increased by 17% to €1.25 billion. Growth was driven by apartments and houses, supported by rising average prices in both segments. The land market showed uneven performance: activity in land fields declined, while values increased due to price growth, and land plots recorded a decline in both volume and value.

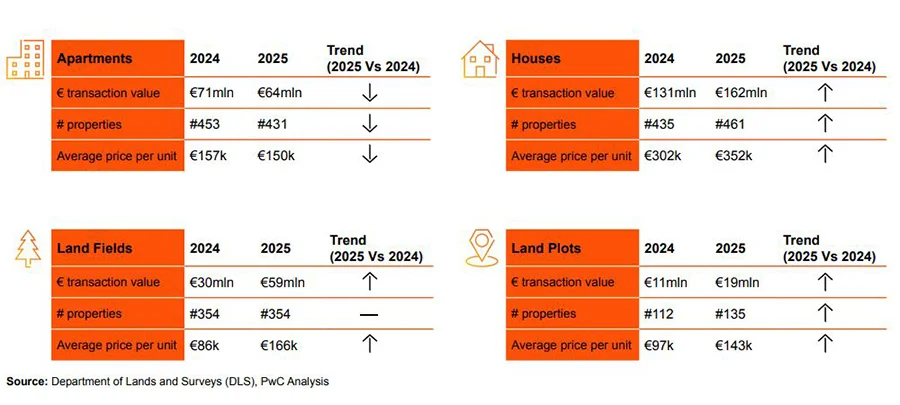

Famagusta recorded a 4% increase in transactions to 1,441 and the strongest growth in total value, up 27% to €0.32 billion. Growth was largely driven by land assets. Strong momentum was observed in land fields, where values increased sharply despite stable volumes, as well as in land plots, where both value and average prices increased. The residential segment developed more moderately, with slight growth in houses and a decline in apartments from 453 to 431 transactions and from €71 million to €64 million. Average prices also declined to €150k.

Advantages and risks of the Cyprus real estate market for investors

Analysts at International Investment note that the Cyprus real estate market in 2025 remains attractive due to rising transaction values, a strong residential segment, and stable foreign demand. Additional support comes from a developed market for both resort and urban property, ensuring liquidity in key regions.

Key strengths include stable demand for residential assets, where apartments and houses account for the bulk of transactions, as well as continued price growth in selected segments. In several regions, investment capital remains highly concentrated, particularly in Limassol and Paphos, supporting overall price and turnover levels.

At the same time, the regulatory environment is becoming increasingly strict. Authorities are gradually revising real estate rules, tightening transaction oversight, and aligning the market with broader European standards. This is already reshaping investment strategies and increasing uncertainty for some market participants.

Predictability of returns is decreasing: tighter regulation restricts certain investment models, while previous advantages are gradually narrowing. Legislative changes have already led to reassessment of investor statuses, including cases of residency and citizenship revocations.

The Cyprus real estate market remains active but is becoming more controlled and less flexible. Entry costs are relatively high and require significant administrative procedures. These factors increasingly push investors to consider alternative markets, including Georgia, which offers easier entry conditions, lower taxes, no restrictions for foreign buyers, and higher rental yields compared to many countries worldwide.