Fed Split Revives Threat of Higher Rates

Fed Split Revives Threat of Higher Rates

Reviews Expose Argentina’s Tourism Weaknesses

Reviews Expose Argentina’s Tourism Weaknesses

Bank Indonesia Expands Support for Rupiah

Bank Indonesia Expands Support for Rupiah

Central Banks Return to Gold After Weak Start

Central Banks Return to Gold After Weak Start

Dubai Real Estate Market Slows Amid Middle East Conflict

Dubai Real Estate Market Slows Amid Middle East Conflict

Egypt launches digital visa-on-arrival system at Cairo International Airport

Egypt launches digital visa-on-arrival system at Cairo International Airport

Record rise in prices for resale housing in Spain

Spain continues to see a significant increase in resale housing prices, which in April 2026 reached new all-time highs, according to Idealista. The average price rose by 16.9% compared to the same month in 2025, reaching €2,748 per sq. m. The increase was recorded in almost all regions of the country, reinforcing signs of a sustained overheating in the housing market and extending the upward trend of recent months.

Over the past three months, prices increased by 3.7%, and by 1.5% compared to March. The index methodology is based on the analysis of property listings, excluding atypical offers and properties with abnormal prices. It also includes houses and apartments actively present in the market, while the final figure is calculated using the median.

Regional dynamics of housing prices in Spain

Prices increased across all autonomous communities without exception. Murcia recorded the strongest growth, with a 23% year-on-year increase. It was followed by Cantabria (+19.2%), Asturias (+17.7%), and Andalusia (+17.6%).

Above-average increases were also recorded in Valencia (+15.4%), Catalonia (+14.1%), Madrid (+13.5%), Aragon (+13.3%), and the Basque Country (+13.2%). More moderate growth was seen in Castile and León (+9.1%), La Rioja (+9%), Galicia (+8.8%), and the Balearic Islands (+8.6%).

The most expensive regions remain the Balearic Islands at €5,252 per sq. m and Madrid at €4,707. They are followed by the Basque Country (€3,534), the Canary Islands (€3,283), Catalonia (€2,890), and Andalusia (€2,852). The most affordable regions are Extremadura (€1,071), Castile-La Mancha (€1,091), and Castile and León (€1,323).

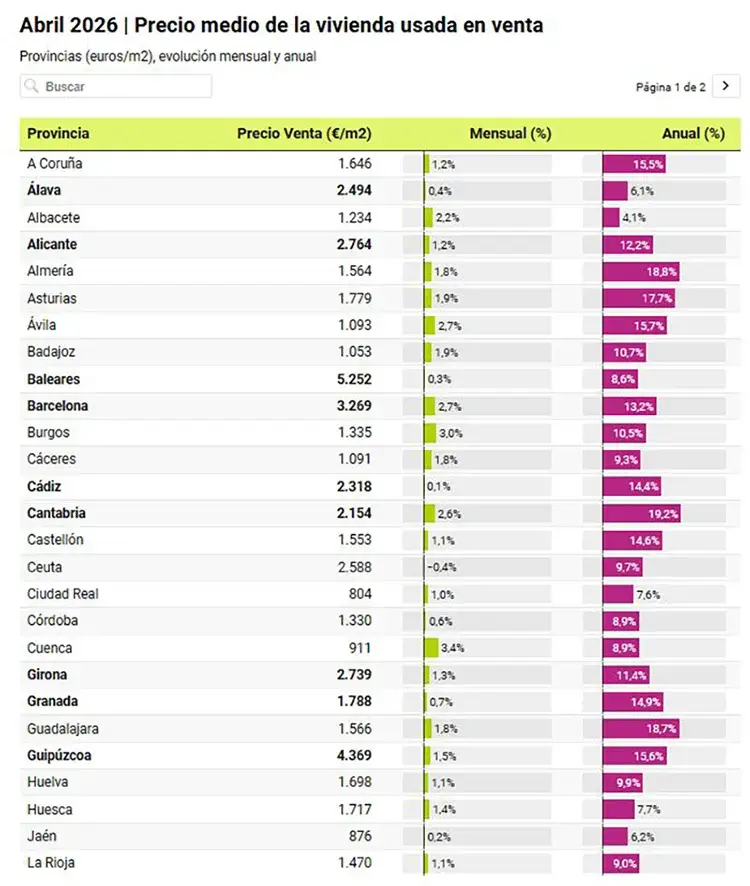

Provinces: sharp price jumps in the southeast and central regions

At the provincial level, price growth was recorded in 48 out of 50 provinces. The only exceptions were Ourense (-1.9%) and Soria (-1.3%). The strongest increases were seen in Valencia (+24.1%), Murcia (+23%), Toledo (+20.5%), Cantabria (+19.2%), and Almería (+18.8%). Major markets also saw growth, with Madrid up 13.5% and Barcelona up 13.2%.

The highest housing prices remain in the Balearic Islands at €5,252 per sq. m. In Madrid, property is priced at €4,707. Other high-value locations include Gipuzkoa (€4,369), Málaga (€4,121), Santa Cruz de Tenerife (€3,434), Biscay (€3,394), and Barcelona (€3,269). The lowest prices are recorded in Ciudad Real (€804), Jaén (€876), and Cuenca (€911).

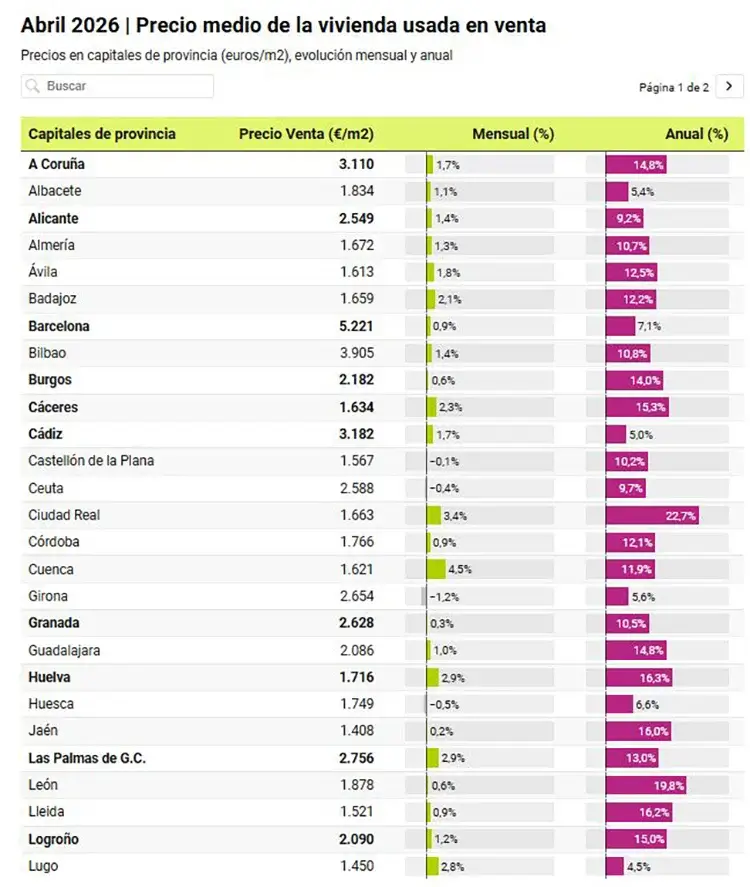

Price growth in Spanish capitals

All provincial capitals in Spain recorded increases in resale housing prices. The strongest rise was seen in Ciudad Real, up 22.7% year-on-year. It was followed by León and Murcia (both +19.8%), Salamanca (+17.5%), and Pontevedra (+17.4%).

Among major cities, growth is more moderate. The highest increase is in Valencia at 12.3%. In Bilbao, resale housing rose by 10.8%, and in Málaga by 10.1%. More moderate increases were recorded in Barcelona (+7.1%) and in Seville and San Sebastián (both +7.4%).

San Sebastián remains the most expensive city in Spain at €6,393 per sq. m, followed by Madrid (€5,960) and Barcelona (€5,221). The most affordable cities include Zamora (€1,370), Jaén (€1,408), and Lugo (€1,450).

Changes in Spain’s real estate market

The Spanish property market is gradually shifting in its demand structure. A year ago, investment-driven transactions accounted for more than 50% of purchases, while now they represent around one-third. At the same time, the share of purchases for primary residence is rising to 20.8%, along with an increase in transactions linked to changes in main housing.

This shift is accompanied by a tightening rental market, driven in part by a shortage of supply linked to stricter regulations.

Rising housing prices are pushing authorities toward a large-scale sector reform. A €7 billion programme for 2026–2030 has already been prepared. It aims to expand the stock of affordable housing and increase state involvement in market regulation. Funds will be directed to new construction, renovation of existing housing stock, and support measures for citizens, including rental and purchase assistance, as well as targeted programmes for young people.

Analysts at International Investment note that the market is becoming less investment-driven, while competition for housing in major cities continues to intensify. In conditions of limited supply and rising prices, pressure increases both on buyers and tenants. Future dynamics are expected to depend less on investment demand and more on real household needs and the pace of housing stock expansion.