Dubai ready home sales fall to lowest level

Dubai’s residential real estate market continues to cool after several years of strong growth. In April 2026, prices declined for the second consecutive month, although the pace of the downturn slowed noticeably compared to March, according to consulting firm ValuStrat. The apartment segment has largely stalled, while the villa market has also been partially affected by the downturn.

Correction in Dubai’s property market

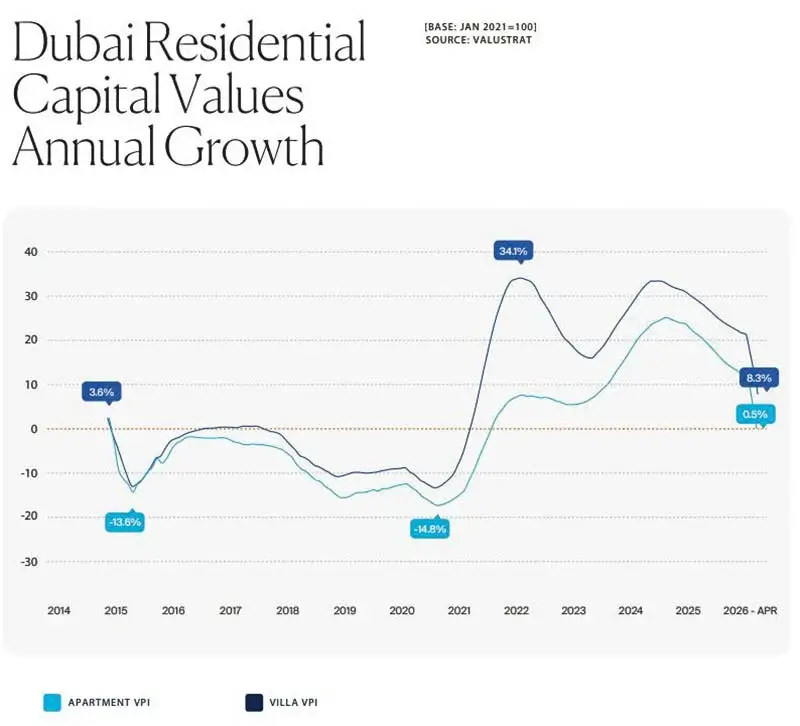

Dubai’s residential Property Price Index stood at 224.9 points in April, based on a benchmark of 100 in January 2021. The index fell by 1.9% over the month, compared to a sharper 5.9% decline in March. Despite the correction, annual performance remains positive, with growth of 5.3%.

The most resilient communities included in the ValuStrat Price Index (VPI) recorded no price declines in April, while most other locations continued to lose value. The weighted average residential price in Dubai reached AED 1,545 per square foot (around $421), or approximately AED 16,600 per sq. m ($4,500 per sq. m). The average property value is estimated at AED 3.45 million ($939,000).

Dubai apartments lose momentum

Apartment prices fell by 6.3% in March and by a further 2.2% in April. Annual growth slowed to just 0.5%. Prices in Burj Khalifa declined by 10.4% year-on-year, Jumeirah Beach Residence by 5.9%, and Town Square by 4.3%.

Some areas, however, continue to show growth. The strongest performance was recorded in Dubai Silicon Oasis and Remraam (+12.4%). Other leading performers included DIFC, Jumeirah Village Triangle, and Dubai Sports City.

Apartment prices in older freehold areas remain 72% above post-pandemic levels, but are still around 6% below the 2014 market peak.

Off-plan sales down 14%

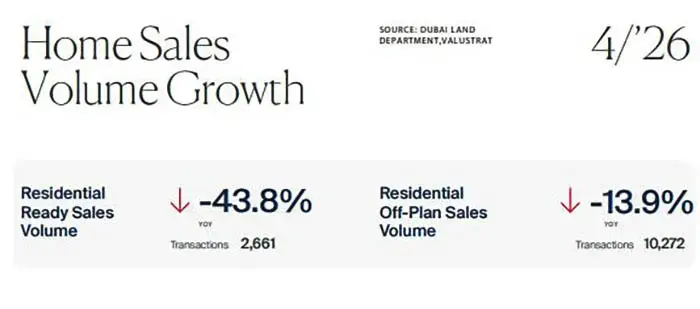

Registrations of off-plan transactions increased by 4% month-on-month, but were 13.9% lower year-on-year. This segment accounted for 79% of total residential sales in the emirate. ValuStrat notes that some transactions may have been agreed before the geopolitical crisis that began on February 28.

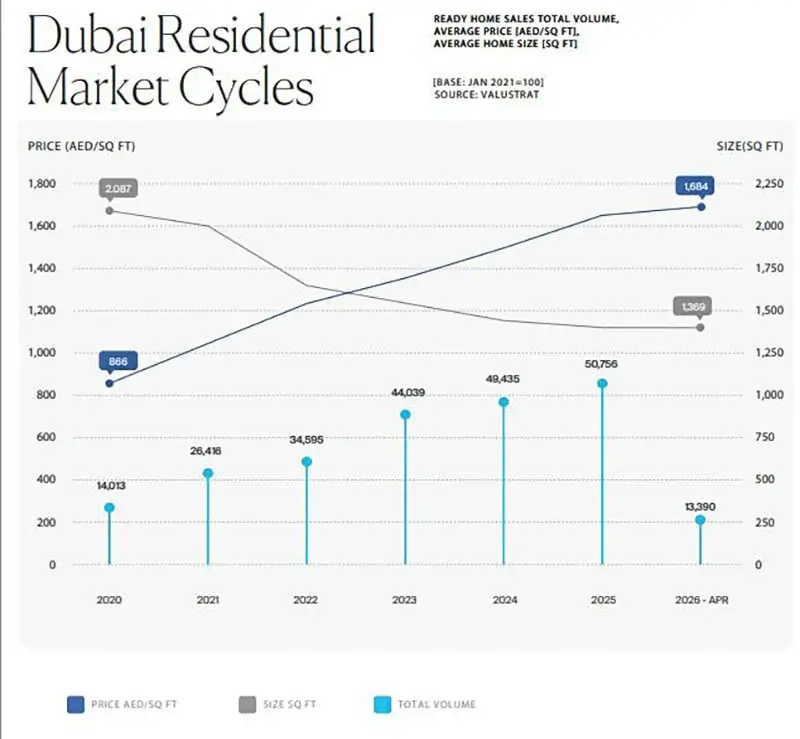

At the same time, ready property sales continue to decline. The number of transactions fell by 4.2% month-on-month and by 43.8% year-on-year, a record-low level for the market.

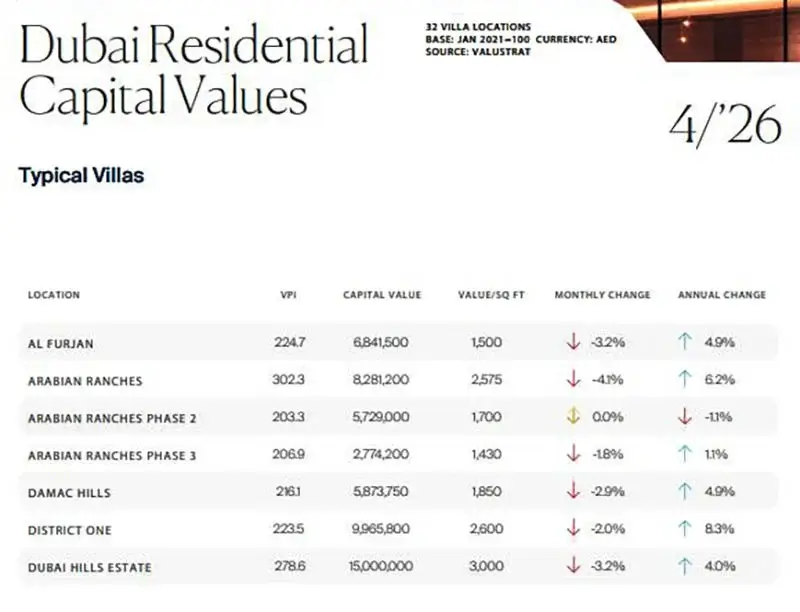

Where villa prices are falling in Dubai

Villa prices in Dubai declined by 1.7% in April compared to March, although annual growth remained strong at 8.3%. Price declines were limited to International City, Arabian Ranches Phase 2, and Victory Heights.

At the same time, villa prices rose significantly in several prime communities: Jumeirah Islands (+24.5%), The Meadows (+14.9%), Emirates Hills (+14.6%), Palm Jumeirah (+12.3%), and Jumeirah Village Circle (+11.4%).

According to ValuStrat, villa prices in mature communities are now on average 196% above post-pandemic levels and around 80% higher than the 2014 market peak.

Premium segment remains active

Despite the broader market slowdown, high-end real estate continues to attract buyers. In April, 16 ready-property transactions above AED 30 million ($8.2 million) were recorded, including four deals exceeding AED 50 million ($13.6 million). The most expensive purchases were concentrated in Palm Jumeirah, Dubai Hills Estate, Al Barari, Jumeirah Islands, Arabian Ranches, Jumeirah Golf Estates, and DIFC.

By developer volume, Emaar led the market with a 14.3% share, followed by Damac (12.1%), Ellington (5.5%), Binghatti (4.8%), Sobha (4.3%), and Nakheel (2.8%). In the off-plan segment, the most active projects were in Damac Islands, Dubailand Residence Complex, Jumeirah Village Circle, Damac Lagoons, and Dubai Creek Harbour.

In the secondary market and ready-home segment, activity was concentrated in Jumeirah Village Circle, Business Bay, Discovery Gardens, Dubai Marina, Arjan, and Damac Hills 2. City Walk also recorded a monthly transaction record for ready properties.

Geopolitics weighs on demand

The Middle East conflict has negatively impacted Dubai’s property market. In March, the Dubai Land Department reported a nearly 20% drop in sales volume to AED 37 billion ($10 billion), marking the sharpest monthly decline since the pandemic.

Sellers have increasingly revised pricing expectations. More than 2,800 properties saw price reductions totaling AED 1.7 billion ($463 million), with discounts ranging from 10% to 50%. Some properties were repriced multiple times.

The most pressure has been observed in the off-plan segment, where payment deferrals have also increased. In the secondary market, more than 300 properties have undergone repeated price cuts since the beginning of the cooling cycle. Villas were also affected, including a four-bedroom property in La Mer, which dropped from AED 110 million ($30 million) to AED 85 million ($23 million), and a villa in Arabian Ranches, which fell from AED 8.5 million ($2.3 million) to AED 7.4 million ($2 million).

Cooling reshapes economic expectations

The property correction is increasingly influencing broader economic expectations in Dubai. Citi analysts have revised their population growth forecast to just 1% in 2026, with annual growth of around 2.5% thereafter, significantly lower than during the boom period.

S&P Global also suggests that some wealthy expatriates may reconsider their plans to remain in the UAE. Rising geopolitical tensions have already affected investor sentiment, with Dubai and Abu Dhabi stock markets losing around $120 billion in market capitalization since the conflict began.

Analysts at International Investment note that the UAE’s attractiveness is still supported by long-term visa programs and pro-investment policies aimed at attracting capital, business, and skilled professionals. However, the conflict has reshaped perceptions of regional security, with intermittent hostilities continuing and peace negotiations yet to deliver a lasting agreement. As a result, some investors are adopting a wait-and-see approach or exploring alternative destinations.

Against this backdrop, interest is increasing in countries not involved in military conflicts and showing stable economic performance. One such market is Georgia, which also offers relatively easy market entry conditions and high yields, particularly in the premium hotel real estate segment, attracting both private and institutional investors.