Foreign Stays Lift Estonia’s Tourism Recovery

Foreign Stays Lift Estonia’s Tourism Recovery

Greece’s Golden Visa: Applications Fall 25%, Backlog Drops 7.3%

Greece’s Golden Visa: Applications Fall 25%, Backlog Drops 7.3%

Indonesia’s Housing Market: Sales Decline, Prices Stagnate

Indonesia’s Housing Market: Sales Decline, Prices Stagnate

Swiss Tourism Growth Remains Concentrated

Swiss Tourism Growth Remains Concentrated

Bulgaria Proposes Stricter Permanent Residence Rules

Bulgaria Proposes Stricter Permanent Residence Rules

Strong UK GDP Masks Weak Economic Momentum

Strong UK GDP Masks Weak Economic Momentum

End of the Price Rally: Dutch Housing Market Cools Down

Rising mortgage rates, worsening housing affordability and increasing geopolitical uncertainty are reshaping the Dutch real estate market. Analysts at RaboResearch expect price stabilisation, fewer transactions and a continued cooling in buyer activity.

Housing Price Growth in the Netherlands Slows

General Downward Trend

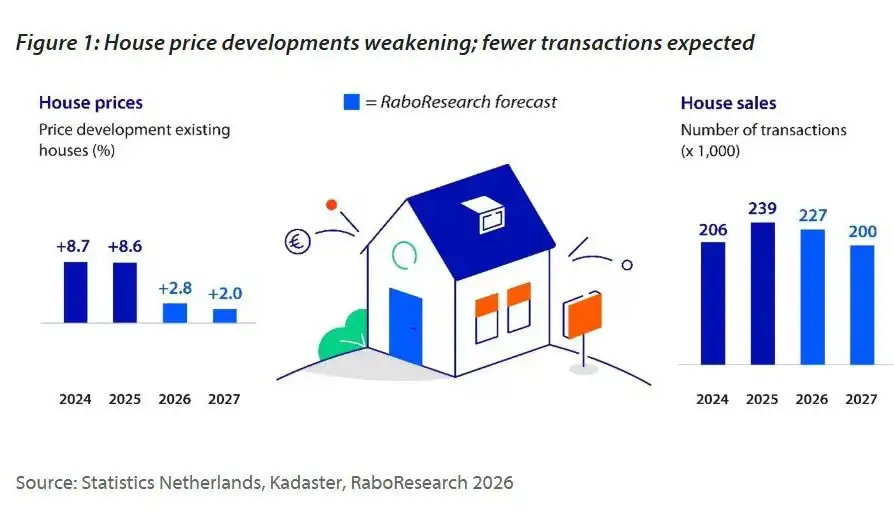

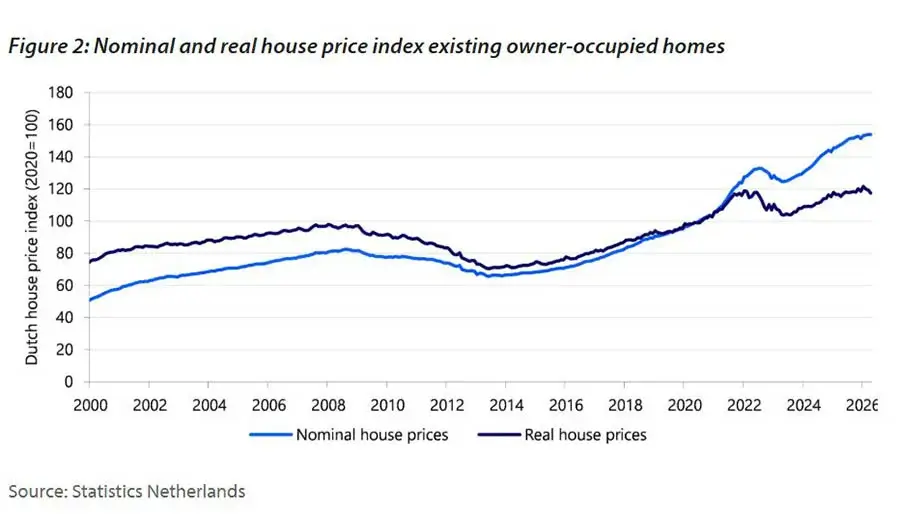

The Dutch housing market is losing momentum. After several years of rapid growth, prices have largely stopped rising, while buyer activity is declining. In April, prices for existing homes remained unchanged compared to March, while annual growth stood at 4.3%. This is significantly below the peak in November 2024, when prices were 11.9% higher year-on-year.

When adjusted for inflation, the picture is even weaker. Real housing prices increased by only 1.8% over the year, effectively returning to levels seen at the beginning of the energy crisis.

According to RaboResearch, prices are expected to remain broadly stable in 2026. However, the annual average will still show a 2.8% increase due to carry-over effects from 2025. In 2027, analysts expect more moderate growth of around 2%.

Regional Developments

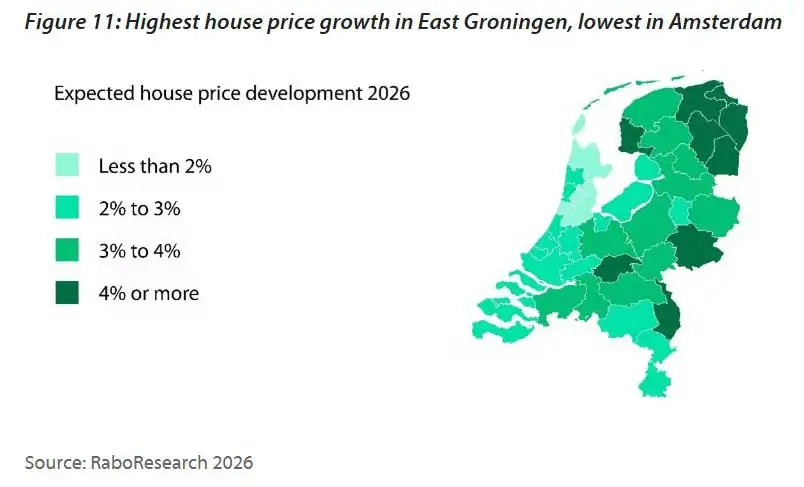

The weakest dynamics are seen in Greater Amsterdam and surrounding areas. In the first quarter, house prices in this region rose by just 2.4% year-on-year, broadly in line with inflation. In real terms, prices were virtually flat.

In contrast, eastern parts of the country continue to show stronger growth. East Groningen recorded a 9% increase in the first quarter. This region has consistently outperformed others in recent years. Meanwhile, previously strong regions are losing momentum: annual price growth slowed to 4.7% in Utrecht and 3.7% in Flevoland.

RaboResearch attributes these differences primarily to supply conditions. Large cities are seeing increased inflows of former rental properties, which limits price growth. In less urbanised regions, supply remains tighter, keeping upward pressure on prices.

Buyer Behaviour Becomes More Cautious

Weaker demand is becoming increasingly visible. Higher mortgage rates and elevated prices are reducing affordability, while geopolitical uncertainty is prompting potential buyers to delay decisions.

Although these effects are not yet fully reflected in official statistics, early signals are already visible. More than one-third of NVM real estate agents report that buyers have become more cautious: they take longer to decide, are less willing to take risks and schedule fewer property viewings. At the same time, the number of enquiries per listed property is declining.

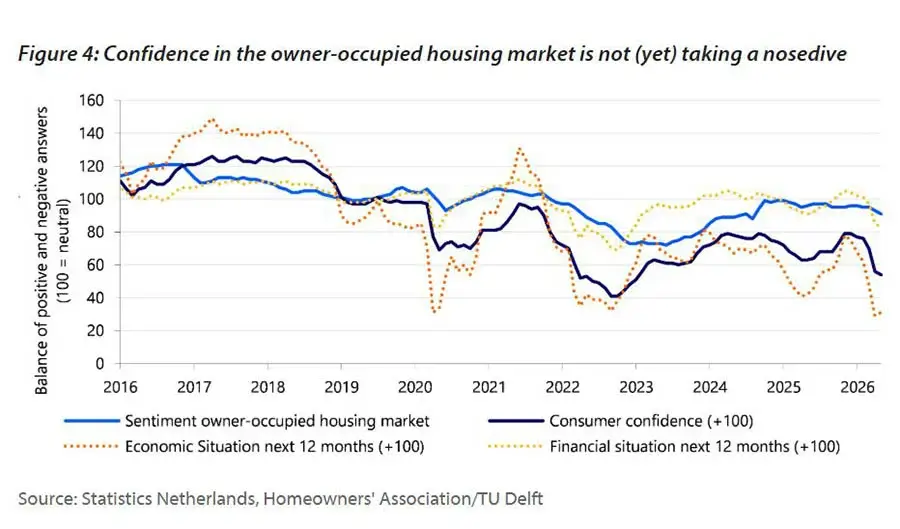

Market sentiment has also weakened, although analysts do not see a sharp deterioration in confidence. According to RaboResearch, confidence in the housing market remains significantly higher than confidence in the broader economy. Economists Carola de Groot and Stefan Groot note that expectations regarding personal income are more important for housing decisions than general economic sentiment. This is why previous crises, including the pandemic, did not lead to a severe housing downturn. The exception was the energy crisis, when rapidly rising mortgage rates did trigger a price correction.

Fewer Housing Transactions Ahead

The Dutch housing market is gradually losing momentum in terms of transactions. In 2025, around 239,000 housing deals were concluded. RaboResearch expects this to fall to 227,000 in 2026 and further to 200,000 in 2027.

In recent years, the market was supported by a wave of former rental property sales, but this trend is now fading. Over the past four quarters, owners sold nearly 39,000 such properties, although net sales have started to decline for the first time since 2023. Most investors planning to exit this segment have likely already done so.

Supply remains elevated: listings on the Funda platform are more than 18% higher than a year earlier. However, growth is slowing. Around 244,000 properties changed hands over the past 12 months, but momentum is weakening, especially in the apartment segment, which has been heavily influenced by former rental stock.

Analysts expect supply to decline in the coming years as the wave of investor sales fades and new construction slows. At the same time, some potential buyers are leaving the market due to worsening affordability.

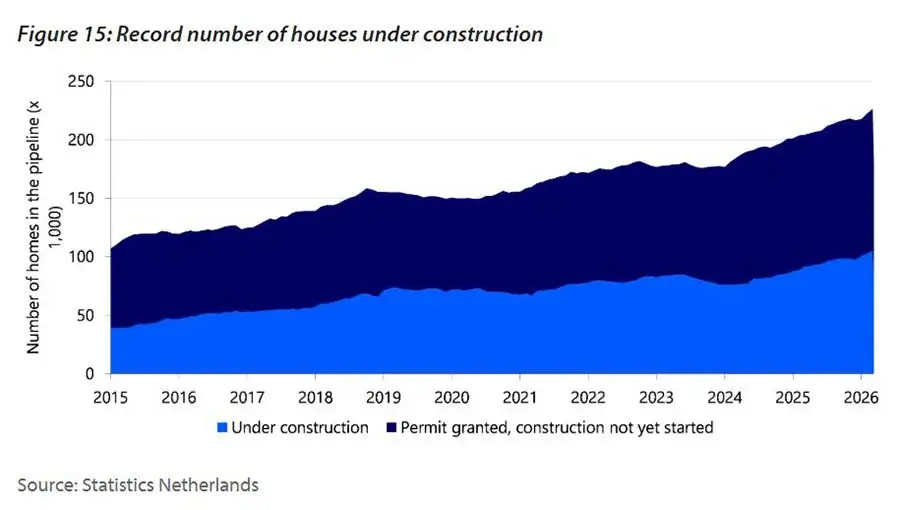

Construction Sector Loses Stability

The Dutch housing construction sector remains under pressure and shows no sustained recovery. After three years of decline, a slight increase in completed homes is expected in 2026, driven largely by projects already in the pipeline.

However, this recovery is likely to be temporary. Structural constraints continue to weigh on the sector: grid congestion, long development timelines, rising material costs and higher interest rates. These factors slow both new project starts and project completion.

Additional pressure comes from declining new-build sales. In the first months of the year, 12% fewer new homes were sold compared to the same period last year. Apartments are particularly affected, as supply often fails to match buyer expectations. Many transactions fall through due to high interim costs and complex financing structures.

Regulatory changes in the rental market and rising costs are also reducing investor appetite for new developments, particularly in the build-to-rent segment. Overall, these factors point to subdued construction activity beyond 2026, making the target of 100,000 new homes per year increasingly unlikely in the near term.

Dutch Economy

The broader economic environment is becoming less supportive for housing. Escalation of the Middle East conflict is affecting energy markets and feeding through into oil and gas prices, inflation and interest rates.

RaboResearch expects weaker GDP growth in the Netherlands: 1.0% this year and 0.8% next year. Unemployment is projected to rise gradually to 4.2% in 2026 and 4.5% in 2027. Inflation is expected to remain elevated at 3.0% and 3.9% respectively, supporting wage growth but also increasing cost-of-living pressures.

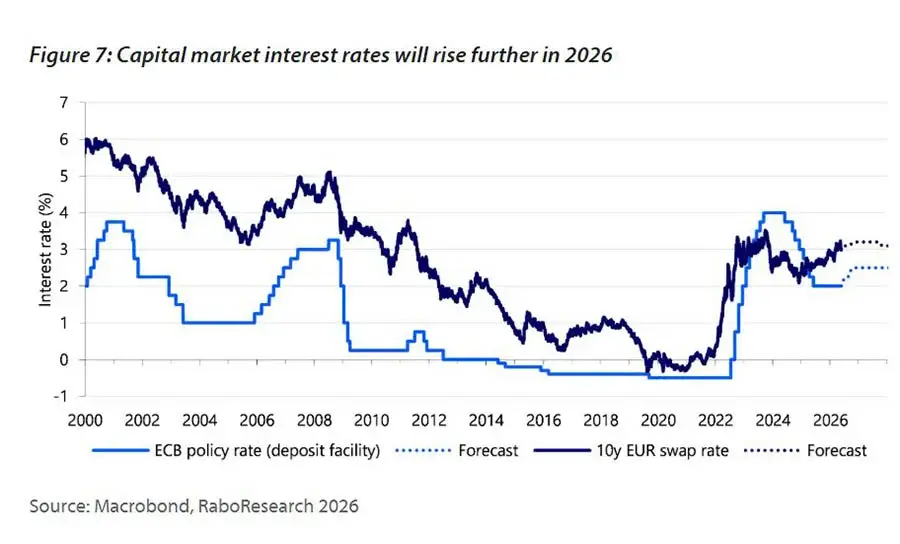

Capital market yields have risen since the start of the year, directly affecting mortgage rates. As a result, borrowing costs continue to increase despite competitive pressure among lenders.

Housing Affordability Remains Limited

Wage growth partially offsets the impact of higher interest rates. RaboResearch expects salaries to rise by 4.3% in 2026 and 4.0% in 2027, above long-term averages.

In practice, however, this only leads to a modest improvement in affordability. In 2026, households with two average incomes will be able to borrow slightly more than in the previous year. By 2027, this effect will largely be offset by higher interest rates.

Analysts also note that maximum borrowing capacity is highly sensitive to interest rate thresholds, meaning even small changes can lead to noticeable jumps in available mortgage amounts. Outcomes also vary significantly across households depending on guarantees and loan-to-value ratios.

Outlook: Slower Market Phase Ahead

Analysts at International Investment note that slower economic growth, rising interest rates, constrained supply and weaker demand are shaping a more subdued trajectory for the Dutch housing market.

After years of rapid expansion, the market is entering a phase of lower momentum. Prices are no longer accelerating as before, and transaction volumes are declining. Regional differences remain significant, while market dynamics are increasingly driven by interest rates and supply conditions.

In the coming years, the market is expected to be more stable but less dynamic, without the sharp price surges seen in previous cycles. For investors, this means rapid capital appreciation can no longer be treated as a baseline scenario, while careful analysis and longer investment horizons become increasingly important.