Belgium Construction Sector Gradually Stabilises

Record Bankruptcies Weigh on Belgian Construction Market

Belgium remains one of the few European countries where building permits are still declining, although early signs of stabilisation emerged in 2025. Business confidence in the construction sector stayed under pressure throughout the year. A brief improvement at the end of 2025 was followed by renewed weakness at the start of 2026.

At the same time, construction bankruptcies reached a new record high. Smaller and younger firms were disproportionately affected. Nearly three quarters of the companies that ceased operations had been active for less than ten years, highlighting the structural vulnerability of new market entrants in a challenging economic environment.

The creation of new construction firms has also slowed, and the growth rate of active companies has been declining for years. This trend contrasts sharply with increasing housing needs driven by population growth and stricter energy efficiency requirements. As a result, the gap between demand for housing and the sector’s capacity to deliver continues to widen.

Housing Market Recovery Supports Construction Activity

Belgium’s housing market experienced a clear rebound in 2025. Lower transfer taxes, more flexible renovation rules and the permanent 6% VAT rate for demolition and reconstruction projects stimulated residential activity.

This recovery is gradually feeding through to the construction sector. Total production posted a modest increase, and building activity began to stabilise after several years of contraction.

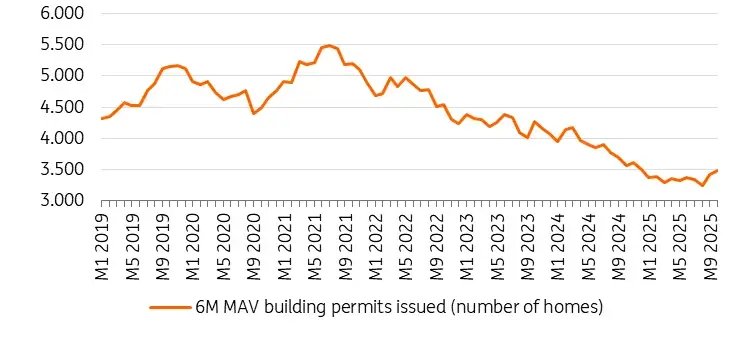

Building permits, which had been falling for years, appear to have reached their lowest point in 2025. Data from Statbel show that the six-month moving average has started to level off, suggesting that the bottom of the cycle may have been reached.

However, higher mortgage rates and slow, complex permitting procedures continue to limit the scope for a rapid rebound.

Construction Growth Forecast for 2026–2027

The outlook points to modest expansion in the coming years. The overall Belgian construction sector is expected to grow by 0.7% in 2026 and 0.8% in 2027.

Building production itself is likely to recover more slowly, with projected growth of 0.2% in 2026 and 0.5% in 2027. This indicates a gradual and fragile recovery rather than a strong cyclical upswing.

The sector remains highly sensitive to macroeconomic conditions, interest rate developments and household investment capacity.

Structural Constraints Continue to Limit Supply

Despite early signs of improvement, structural challenges persist. Building permits remain at historically low levels, particularly for apartment projects. This deepens the mismatch between rising demand for compact and affordable housing and limited new supply.

Demand for new construction remains subdued. Elevated interest rates and still-high material costs continue to weigh on affordability for both households and developers. Although construction material prices have stabilised, they remain well above pre-2022 levels.

Upcoming European climate measures and trade policies could add further cost pressures in the years ahead. This may dampen interest in new projects and contribute to postponed investment decisions.

In this environment, the recovery that began to emerge in 2025 remains fragile. Weak demand and complex administrative procedures continue to constrain the sector, making a strong rebound unlikely unless structural bottlenecks are addressed.

As International Investment experts report, Belgium’s construction sector is gradually moving out of its downturn phase, but sustainable recovery will depend on easing regulatory constraints, stabilising financing conditions and restoring investor confidence.