Stagnant Balance: Buenos Aires Office Market Remains in Limbo

Photo: JLL

During the first half of 2025, the Buenos Aires office market experienced a cautious stabilization. According to JLL, the total net absorption reached 15,897 sq m, while the vacancy rate increased to 18.5%. Rental prices remained nearly unchanged, with an average of $22.7 per sq m per month as of June.

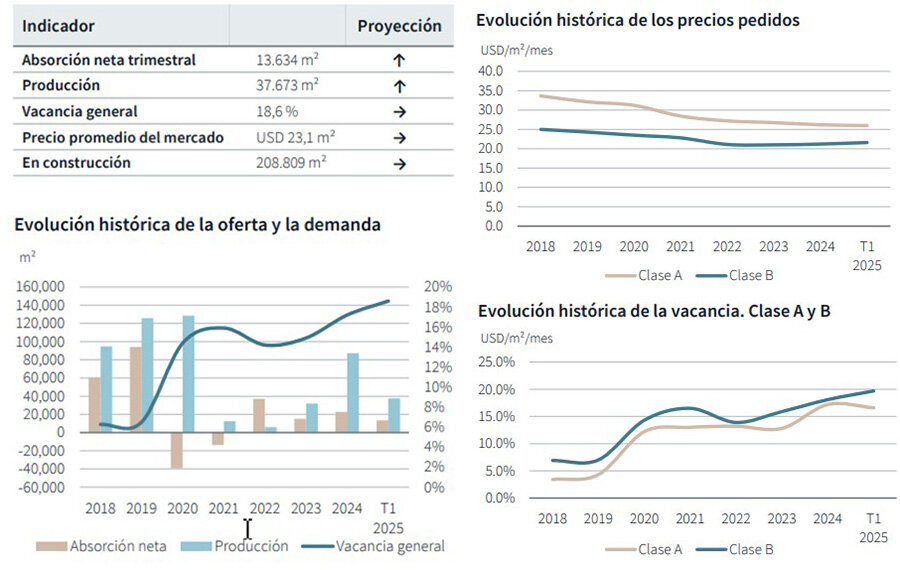

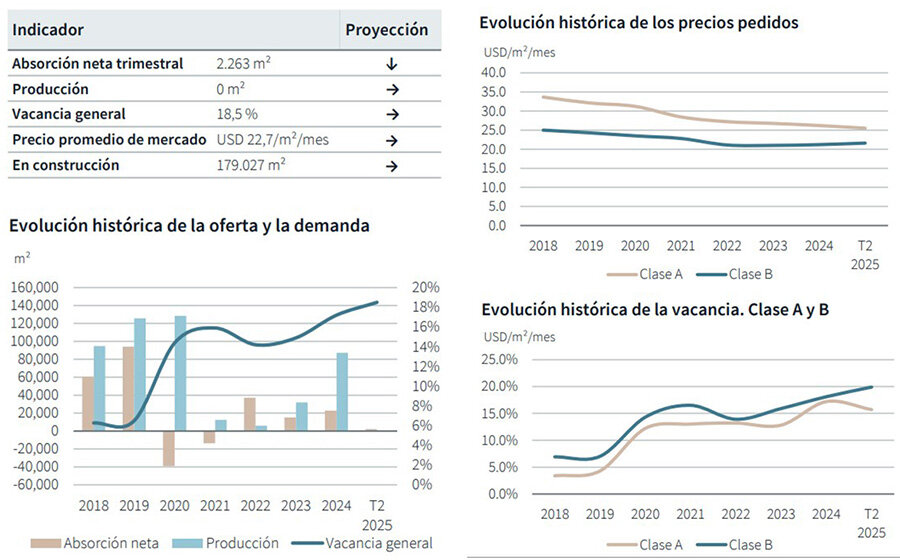

The year began relatively actively: between January and March, 13,634 sq m of office space were absorbed, compared to a negative 7,106 sq m at the end of 2024. However, the pace slowed sharply in Q2, with only 2,263 sq m of net absorption, indicating a plateau and inertia-driven behavior.

Class A offices remained the only stable segment: 5,391 sq m were absorbed in Q1 and 8,674 sq m in Q2. In contrast, Class B offices showed volatility: +8,243 sq m in Q1, followed by –6,411 sq m in Q2, leading to just 1,832 sq m of total net absorption in H1.

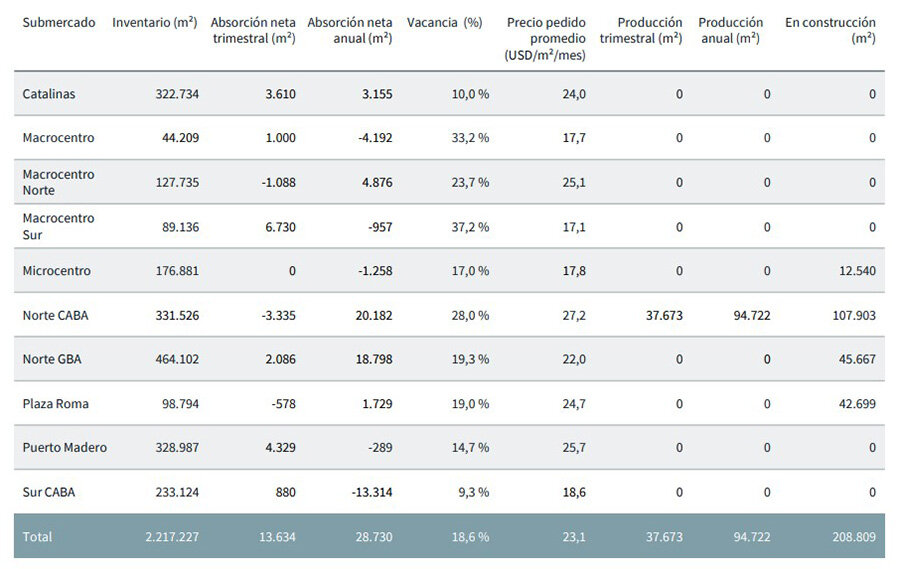

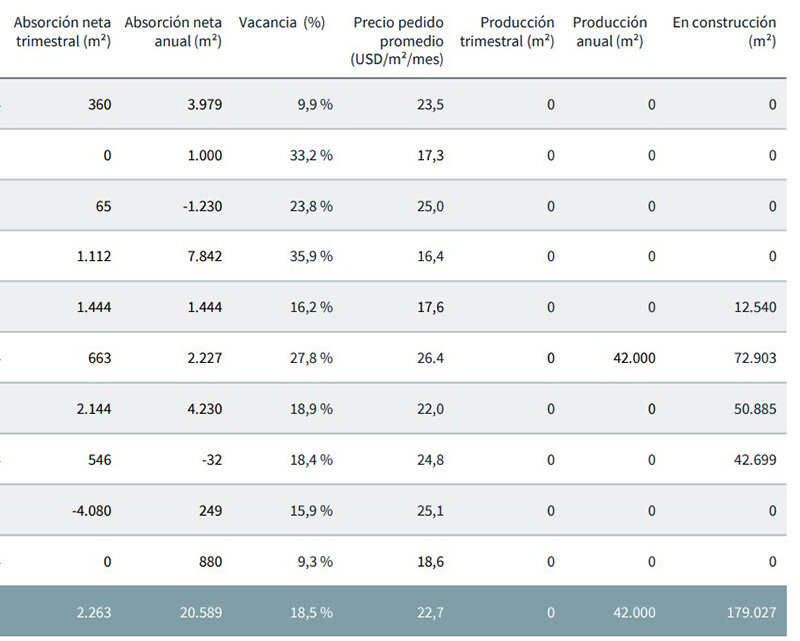

Rental rates were stable. The average in Q1 stood at $23.1/sq m, and $22.7/sq m in Q2. Class A rents declined from $26.0 to $25.5, while Class B remained at $21.6. The highest rates were seen in Norte CABA ($27.2 and $26.4), Puerto Madero, and Catalinas. The lowest were in Macrocentro Sur – $17.1 in Q1 and $16.4 in Q2.

The vacancy rate rose from 17.3% at the end of 2024 to 18.6% in March and stabilized at 18.5% in June. Highest vacancy was in Macrocentro Sur (35.9%), Macrocentro (33.2%), and Macrocentro Norte (23.8%). Lowest levels were in Sur CABA (9.3%) and Catalinas (9.9%).

Inventory increased in Q1 with the delivery of a 37,673 sq m building in Norte CABA, bringing the total to 2,217,227 sq m. No new completions occurred from April to June, and inventory slightly fell to 2,215,726 sq m.

Construction is slowing: from 208,809 sq m under development in early 2025 to 179,027 sq m in summer. The largest pipeline was in Norte CABA (107,903 sq m in Q1, 72,903 sq m in Q2), followed by Norte GBA (45,667 and 50,885 sq m) and Plaza Roma (42,699 sq m). A total of 42,000 sq m of office space were delivered in Q2, all located in Norte CABA.

In Q1, the submarkets with the highest positive absorption were Macrocentro Sur (+6,730 sq m), Puerto Madero (+4,329 sq m), and Catalinas (+3,610 sq m). In Q2, Norte GBA (+2,144 sq m), Microcentro (+1,444 sq m), and Plaza Roma (+546 sq m) led. The most significant negative absorption was in Puerto Madero (–4,080 sq m).

By mid-year, the highest annual absorption was in Macrocentro Sur (+7,842 sq m), followed by Norte GBA (+4,230 sq m), Catalinas (+3,979 sq m), and Microcentro (+1,444 sq m). The biggest losses were recorded in Sur CABA (–12,434 sq m in Q1, +880 sq m in Q2) and Macrocentro Norte (–1,230 sq m).

JLL charts confirm a steady decline in Class A rents since 2018 – from $36 to the current $25–26. Class B decline is less steep, but vacancy remains above 20%. While prices have stabilized, demand remains weak. The market is waiting for new drivers – current trends reflect stagnation rather than recovery.