China’s Property Crisis Increases Risks for Banks

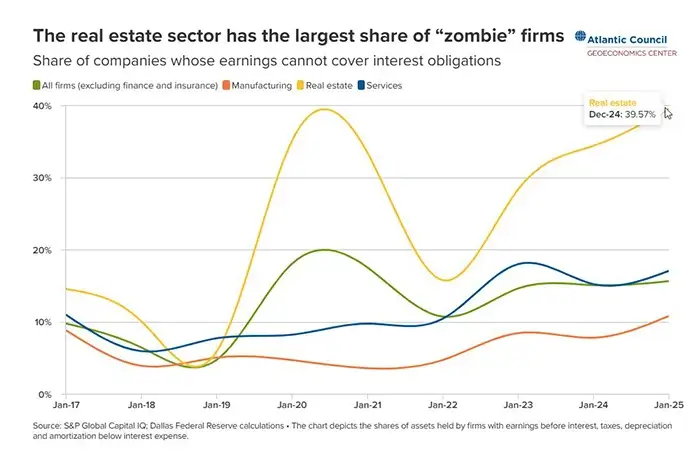

The Share of Non-Performing Loans Has Reached 40%

China’s property crisis has entered its fifth year and is exerting growing pressure on the banking system, regional budgets, and consumer demand. Home sales, prices, and construction volumes continue to decline, dozens of developers have defaulted, and the share of loans to companies whose profits are insufficient to service their debt has reached 40%. These trends raise the likelihood of prolonged stagnation and intensify pressure on the financial sector, analysts at the Atlantic Council note.

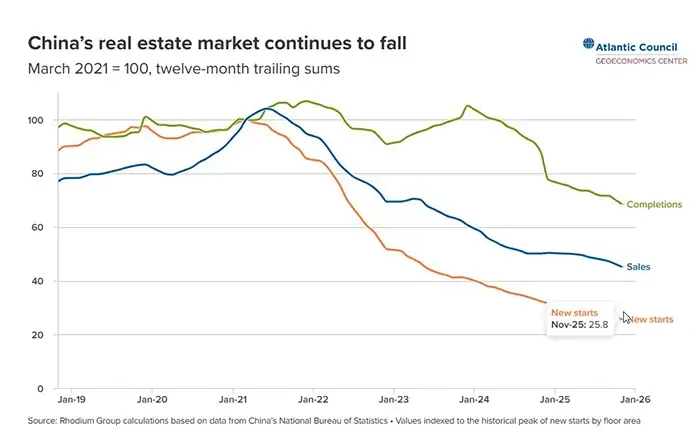

Declining Property Sales in China: 80 Million Vacant Apartments

China’s real estate market continues to show a steady deterioration in key indicators. Sales, prices, housing starts, and completions are falling, while around 80 million unsold or vacant apartments have accumulated nationwide. The fifth consecutive year of decline points to a structural crisis rather than a cyclical correction.

More than 60 major private developers have defaulted on offshore obligations or entered debt restructuring. China Vanke Co., one of the largest state-backed developers, is also facing serious difficulties and has been trying for months to avoid a similar fate. Experts suggest that up to 80% of developers and construction firms could exit the market in the coming years as the sector contracts.

Chinese authorities have effectively acknowledged the end of the previous development model built on high leverage and rapid capital turnover. A transition to a new framework has been announced, with a focus on affordable housing and relative price stability. The sector, which once accounted for roughly a quarter of GDP and a significant share of nonfarm employment, is gradually losing its role as a key growth driver.

The Collapse in Housing Prices

For decades, real estate served as the primary store of household savings in China. Rising prices fostered a sense of financial security and supported consumer spending. After credit tightening in 2021, much of that effect disappeared. According to Macquarie Group, around 85% of the price gains that underpinned household wealth creation have evaporated.

Falling housing values have affected consumer behavior: retail sales have weakened, private investment has declined, and business confidence has deteriorated. Slower domestic demand has become one of the factors weighing on economic growth. Data for the fourth quarter of 2025 confirmed continued weakness in consumer activity.

Boosting domestic consumption remains a stated priority of economic policy. Without at least partial stabilization of the real estate market, that objective becomes more difficult, as housing still occupies a central place in the asset structure of Chinese households.

Zombie Companies and Rising Non-Performing Loans

Key risks are concentrated in the financial system. A study by the Federal Reserve Bank of Dallas shows that in 2024 about 40% of loans to the real estate sector were issued to companies whose operating earnings did not cover interest payments. In 2018, the figure stood at 6%.

This reflects the expansion of so-called zombie companies that continue operating through loan rollovers. Banks prefer to refinance such borrowers rather than recognize losses. The practice delays balance sheet cleanup and locks capital into low-productivity projects.

The issue extends beyond construction. The share of zombie firms across the broader economy has risen to 16%, up from 5% six years ago. Such a structure reduces productivity and limits the potential for a sustained recovery.

Regional Banks, Local Debt, and Shadow Financing

Additional risks stem from the close ties between banks and local government financing mechanisms. A significant portion of credit exposure is linked to entities established to generate revenue for provincial and municipal budgets. Over the past year, the central government has needed approximately $1.4 trillion to refinance accumulated obligations.

AXA Investment previously warned about the complex interconnections between financial institutions, developers, and government entities. This configuration makes the system vulnerable, as even limited disruptions could trigger a chain reaction.

Risks are also rising in the shadow banking segment. In early 2026, Bloomberg reported a crisis in Hangzhou where a shadow lender failed to meet $2.8 billion in obligations to investors. The underlying assets were loans to property developers, some of which had already defaulted. Schemes that once fueled construction sector expansion are now becoming sources of systemic instability, particularly for regional and rural banks.

A Scenario of Prolonged Stagnation

The Dallas Fed study draws parallels with Japan’s debt crisis of the 1990s. Prolonged rollover of bad loans and the survival of inefficient borrowers can distort capital allocation and reduce productivity, potentially locking the economy into extended stagnation.

Harvard economist Kenneth Rogoff and IMF economist Yuanchen Yang also point to similarities with past financial crises. A sustained downturn in real estate exerts broad pressure on both the financial system and overall growth.

Even if China’s largest state-owned banks remain stable, pressure on regional lenders and household confidence could persist for years. Recovery will require reallocating resources, recognizing part of the accumulated losses, and building a new growth model capable of replacing real estate as one of the main drivers of China’s economic dynamism.

Disputes Over Risk Transparency

In its latest financial system review, the IMF stated that assessing systemic risks among smaller banks is complicated by limited public data and restricted access to supervisory information. The report notes that authorities did not disclose institution-specific exposures to local government financing vehicles and property developers, areas considered particularly vulnerable.

Information controls have tightened in recent months. Beijing has restricted the release of certain housing sales data after statistics showed the sharpest decline in 18 months. Oversight of public discussion of housing policy has also increased.

Chinese officials insist that banking risks are under control. Analysts at International Investment note, however, that even under a relatively favorable scenario, the financial system and broader economy could face a prolonged negative impact given the scale of losses and the depth of adjustment.