Translation: Real Estate Markets in Belgium and Luxembourg Shift Focus to Logistics and Housing

In Q1 2025, JLL and UPSI-BVS conducted a survey among real estate investors active in Belgium and Luxembourg. Respondents cited continued uncertainty around interest rates and strict credit conditions, while showing growing interest in logistics, residential properties, and high-ESG-potential assets.

Investment volumes and structure in the real estate markets of Belgium and Luxembourg

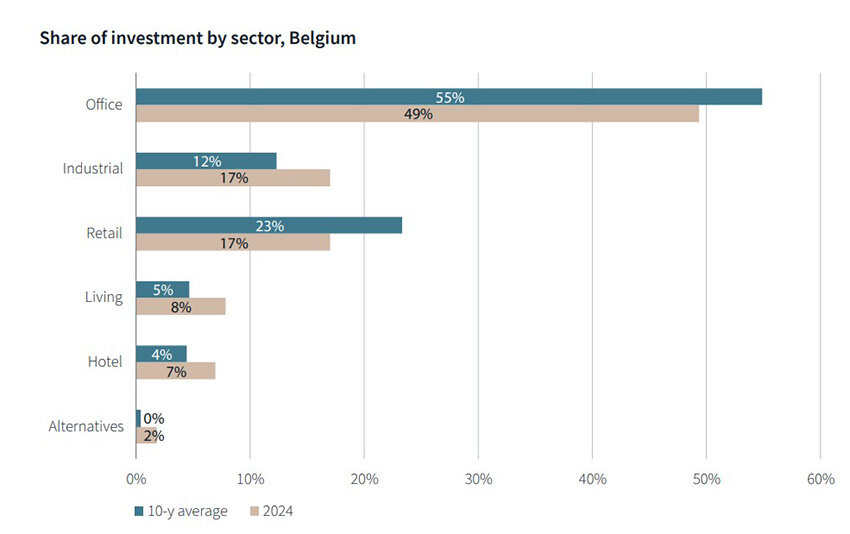

In 2024, real estate investment in Belgium increased by 14% to €3 billion, mainly due to the €850 million City Forward portfolio transaction, which accounted for 83% of office activity. However, offices saw their share fall from 49% to 37% compared to the 10-year average. Residential investments rose from 8% to 17%, logistics from 12% to 23%, and hotels from 2% to 7%. Retail dropped from 17% to 8%, and alternative assets from 10% to just 2%.

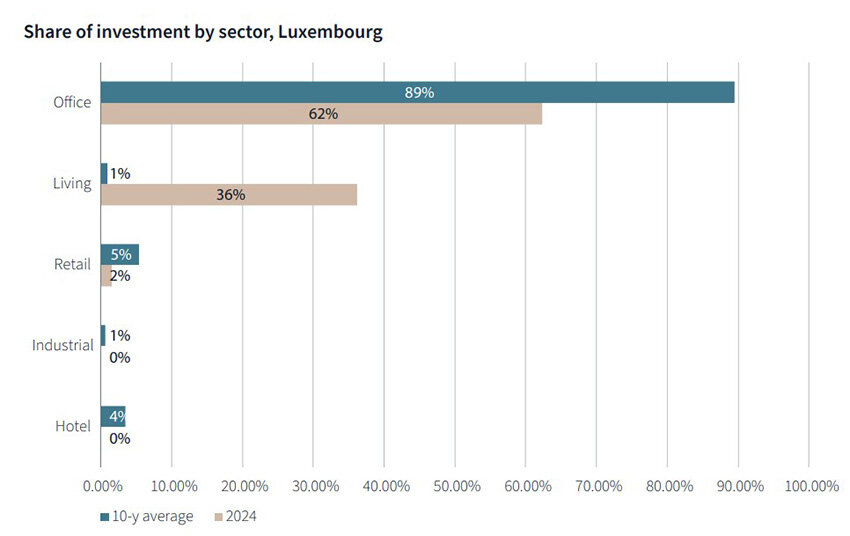

Luxembourg also saw a 14% rise in investments, reaching €606 million. Notably, 89% of this was directed at residential real estate—far above the historical average of 36%. There were no office or logistics deals, sectors that had previously accounted for 62% and 5% respectively. Retail remained stable at 1%.

The share of domestic investors rose significantly: 85% in Belgium (up from 49%) and 50% in Luxembourg (up from 24%). This shift reflects both declining foreign interest and a reallocation of local capital toward defensive assets.

Investor strategies and priorities in Belgium and Luxembourg

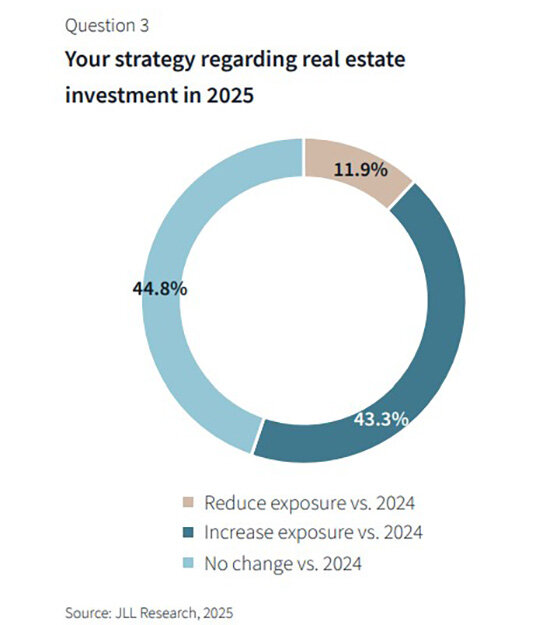

Most investors plan to maintain or increase exposure to real estate in 2025. The preferred deal size is €15–25 million, close to the market average between 2020–2024. Around 30% target €25–50 million deals—typical for logistics (€25M) and office (€37M) assets.

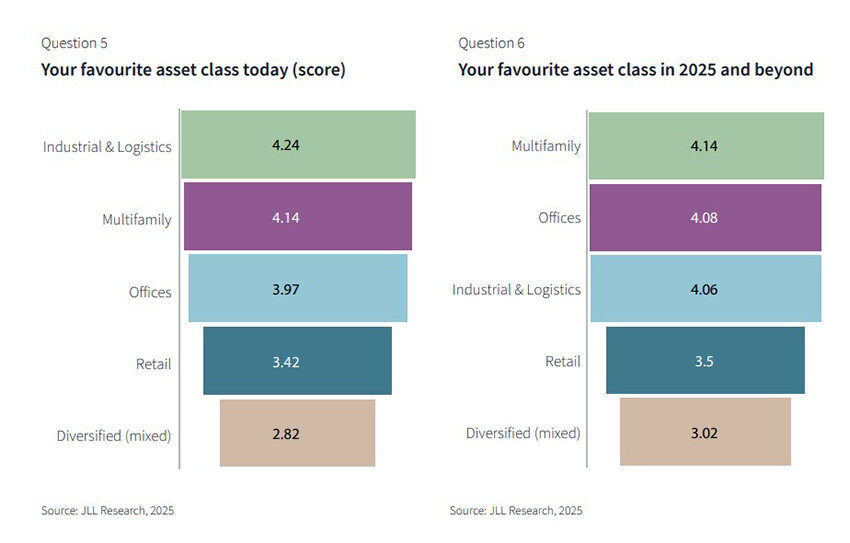

Industrial/logistics remains the most attractive sector, scoring 4.24/5 in short-term appeal due to strong demand, limited supply, and a transparent yield model.

Residential ranks second, scoring 3.97 now and 4.08 long-term—higher than logistics (4.06) and close to offices (4.14). Stability, social relevance, and potential public support drive interest. In Luxembourg, housing already dominates, taking up 89% of 2024’s total investment volume.

Offices remain less attractive for now (2.82/5), but expectations for 2025 indicate recovery (4.14), assuming reduced volatility and streamlined permitting. In Belgium, office permits can take 5–6 years to obtain.

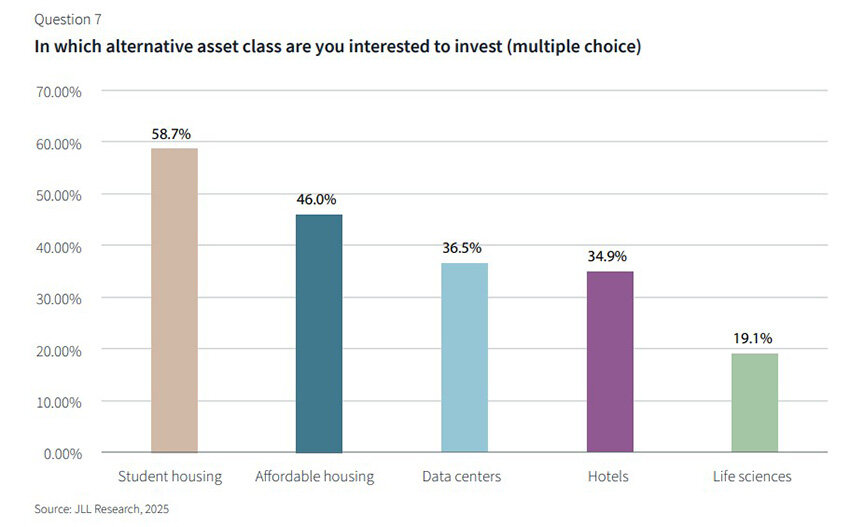

Alternative real estate for investors

When asked about alternative asset classes, 58.7% of investors favored student housing, citing undersupply in cities like Brussels, Antwerp, Ghent, and Leuven. Affordable housing ranked second (46%) as a lower-risk, socially supported investment. Data centers came third (36.5%) due to the expansion of AI and cloud infrastructure.

Although still a minor share of overall volume, these segments are increasingly seen as part of balanced investment strategies, offering resilience and alignment with tech and social trends.

Real estate market outlook

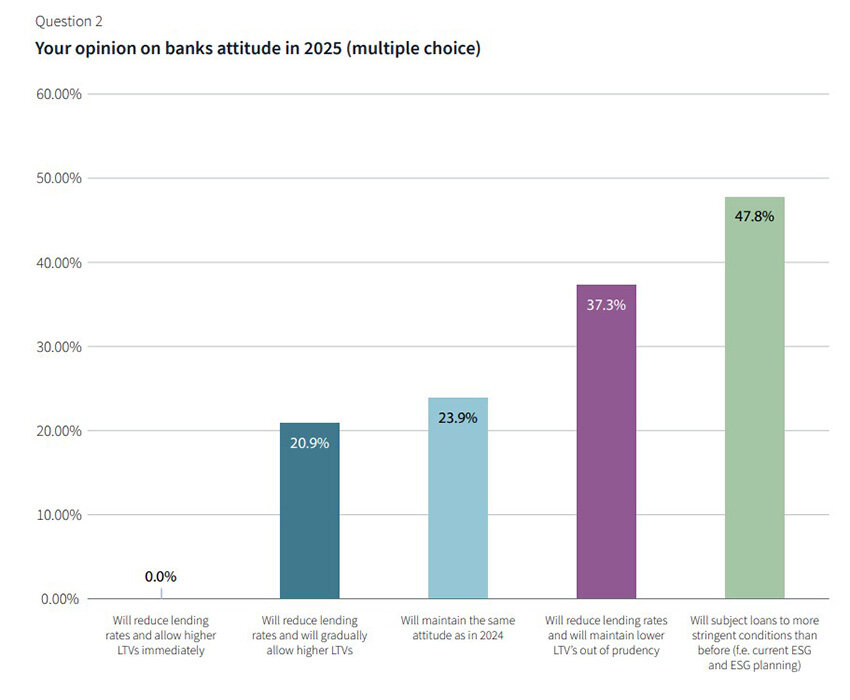

Most investors expect interest rates to fall. Stability is anticipated at 2–2.5% ECB rates, deemed ideal by 41% of respondents. Another 44% favor a drop to 1.5–2%. Banks remain cautious, maintaining low LTVs and prioritizing environmentally compliant projects.

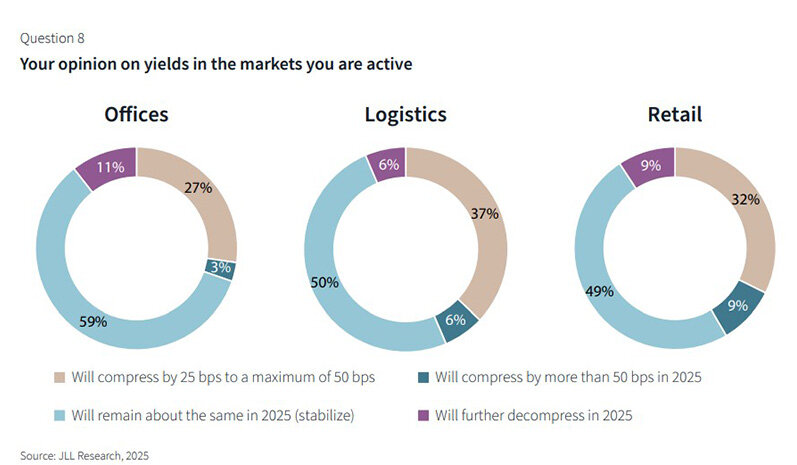

Real estate return forecasts and risks

In the office sector, 59% expect stable yields, while 32% foresee a 25 bps drop. In residential, half see stability, 37% a possible yield compression. Logistics saw a split: 50% expect stability, 27% foresee lower yields, and 9% are optimistic. Retail remains unpredictable.

Top risks include global economic instability and trade tensions, especially after U.S. tariff threats post-April 2025. Administrative delays—like the 5–6 year office permit process in Brussels—remain a major concern. ESG fears and fund withdrawals are now seen as less urgent.