Prices of luxury housing worldwide rose by 3.2% in 2025 — Knight Frank

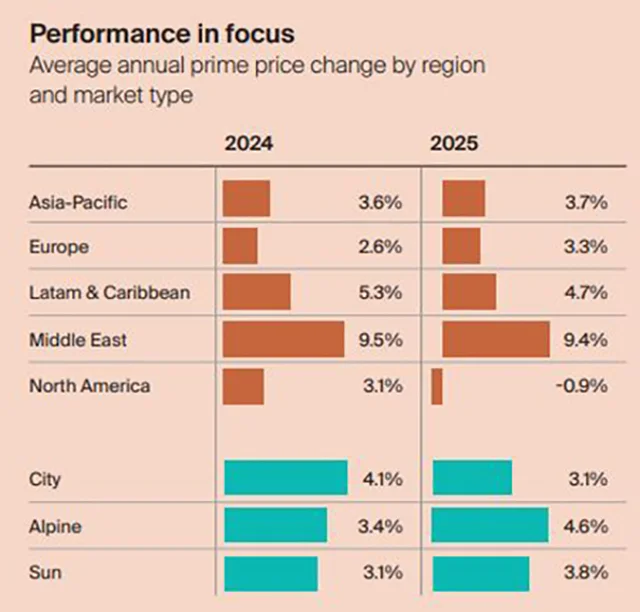

The global luxury residential real estate market increased by an average of 3.2% in 2025, slightly slowing compared to 2024 (3.6%), according to Knight Frank. The prime segment continues to outperform the mainstream housing market, where growth stood at 2.9%. The Middle East led price growth, while North America entered negative territory.

Global dynamics in the luxury real estate market

The Prime International Residential Index (PIRI 100) analyses price dynamics across 100 key prime residential markets worldwide. Price growth was recorded in 73 markets, while 24 experienced declines. The most striking example of growth is Tokyo, where new luxury apartments increased in price by 58.5%. At the same time, declines were recorded in several Chinese cities, in particular in Guangzhou, where the drop amounted to 12.2%, which became one of the most pronounced negative results in the sample.

The Middle East became the fastest-growing region with an increase in prices of 9.4%. In Latin America and the Caribbean, growth amounted to 4.7%, in the Asia-Pacific region — 3.6%, in Europe — 3.3%. North America was the only region with negative dynamics: the average decline amounted to 0.9%. This is primarily due to weakness in Canadian markets and local corrections in the largest cities in the region.

Long-term performance: where luxury housing grew the most

Knight Frank records a significant divergence in the dynamics of prime markets over the past five years. The most notable increase in value was recorded in Tokyo, where prices for new luxury apartments rose by 58.5%. The rise is explained by a shortage of quality supply, low interest rates, and strong demand from buyers in the Asia-Pacific region.

Mumbai also showed strong dynamics (+8.7%). Growth was supported by record transactions in the new-build segment worth over 2 million US dollars and the expansion of domestic demand for high-budget housing. In the United States, Florida markets stand out in particular: cumulative growth in key locations reached 67.1%. Miami became the main centre of capital inflows, transforming from a seasonal destination into a full-fledged international luxury real estate market.

In Europe, one of the most dynamic directions was Portugal (+61.2%). The market was influenced by tax incentives, visa programmes, limited supply, and improved transport accessibility through new direct flights from the US. At the same time, in Auckland prices fell by 8.8% after a period of rapid growth during the pandemic. In London, the decline amounted to 4.7% and is linked to changes in the tax regime for high-net-worth residents, including adjustments to non-dom status.

What $1 million buys in luxury real estate

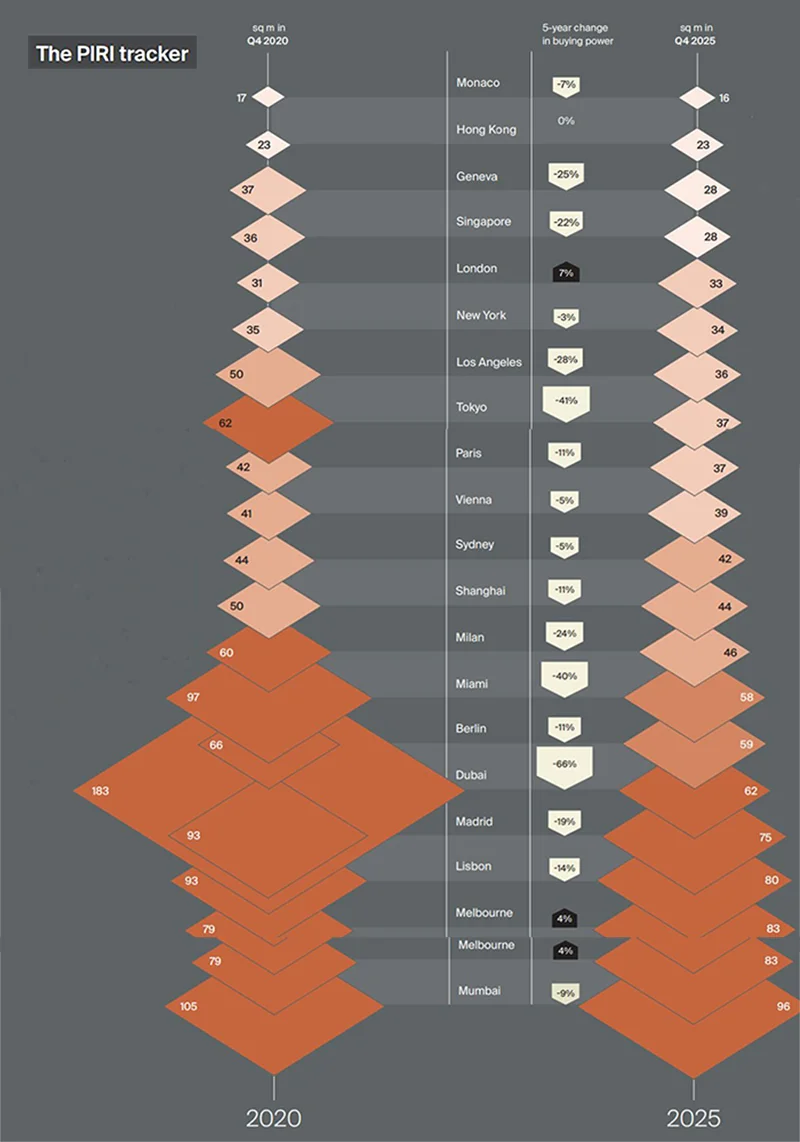

Analysts calculated how many square metres of luxury housing can be purchased for 1 million US dollars in major prime markets worldwide. The most expensive market remains Monaco, where this amount buys only around 16 sq m. In Hong Kong, Geneva, and Singapore, the same budget allows the purchase of 23–28 sq m, in London — 33 sq m, and in New York — 34 sq m. Significantly more opportunities exist in Dubai (62 sq m), Madrid (75 sq m), and Lisbon (80 sq m). Mumbai leads in terms of area — 96 square metres.

The index also shows how purchasing power in this budget segment changed from 2020 to 2025. The sharpest decline was recorded in Dubai — minus 66%, reflecting rapid price growth in the prime segment. A significant decline was also recorded in Tokyo (-41%), Miami (-40%), and Los Angeles (-28%). In Geneva, Singapore, and Milan, indicators also decreased. At the same time, in London the indicator increased by 7%, in Melbourne — by 4%, while Hong Kong remained stable.

North America: rising US prices and Canadian decline

In 2025, luxury real estate prices in North America decreased on average by 0.9%. Pressure on the market is primarily linked to Canada, where rising borrowing costs continue to affect demand in the upper segment.

In New York, prices rose by 0.8%, however the market faces a severe shortage of high-quality turnkey housing. The lack of “ready-to-move-in” properties is particularly noticeable, supporting competition among buyers in the most prestigious locations, including the Upper East Side.

Los Angeles showed growth of 19%, however the ultra-prime segment is experiencing reduced liquidity due to tax initiatives, including Measure ULA — an additional levy on luxury property purchases. This limits activity in the most expensive segment, despite continued interest in select exceptions, including Beverly Hills.

Luxury housing in Aspen increased in price by 2.3%. Here, the third-highest annual sales volume in its history was recorded. This is one of the most stable markets in the region.

Miami declined by 0.5% after several years of strong growth during which the city transformed into an international capital inflow hub. In 2025, foreign investment in residential real estate here amounted to 4.4 billion US dollars.

Canadian cities showed a more pronounced decline: Vancouver lost 7%, Toronto — 7.8%. The main pressure factor was high debt costs, although Toronto retains long-term potential as a centre for the technology and AI sector.

Middle East: inflow of international capital

The Middle East became the leader of the global luxury real estate market, showing average price growth of 9.4%. The main contribution was provided by Dubai, where housing prices increased by 25.1%. In 2025, 500 transactions involving properties worth more than 10 million US dollars were concluded in the city, compared to 113 in 2021, reflecting a sharp expansion of the ultra-prime demand segment.

The market was supported by a steady inflow of international capital and a high concentration of wealthy buyers. The role of Abu Dhabi also increased, forming an alternative destination for buyers oriented towards a more private lifestyle format. This market developed due to demand for restrained and less public assets.

A war in the Middle East, which began on 28 February 2026, sharply changed the situation. Analysts have already calculated that in March, prices in the UAE fell by 5.9% month-on-month — the first decline since 2020. Apartments decreased by 6.3%, villas by 5.8%. Annual growth still remains, but it has slowed significantly. Off-plan transactions (78% of the market) fell by 9.3% month-on-month. In the completed housing segment, a sharp decline was recorded in both calculation formats — minus 37.8% and 34.2%. The region has lost its status as a safe territory for living, leisure, and investment.

Prime residential real estate in the Asia-Pacific region

In the Asia-Pacific region, prices increased by 3.6% in 2025, however dynamics across cities differ significantly. Hong Kong declined by 2.1%, but at the same time recorded growth in ultra-prime activity. In the fourth quarter, the number of transactions above 10 million US dollars reached 81 — the second result among global cities after Dubai.

Singapore continued to show record prices: transactions regularly exceeded 6,000 US dollars per square foot. At the same time, volumes remained limited due to a 60% tax on purchases for foreign buyers. In India, growth in the upper segment is linked to rapid expansion of private wealth, especially in Mumbai.

Australia showed stable demand in the lifestyle segment, including the Gold Coast and Brisbane. Sydney recorded a record 52 ultra-prime transactions in the fourth quarter. In New Zealand, the market remained more restrained: Auckland showed a decline of 5.2% with limited supply and selective demand for premium properties.

Europe: pressure of tax policy and capital redistribution

In 2025, the European luxury real estate market was in a phase of restructuring. London declined by 4.7% after changes in the tax regime for high-net-worth residents, which affected demand structure and increased interest in renting rather than buying. At the same time, a shortage of high-quality properties in the upper segment remained, especially in the most prestigious areas of the city.

Part of the capital was redistributed within Europe towards alternative destinations. Milan showed growth of 0.4%, remaining close to stagnation. Madrid increased by 5%, reflecting stronger interest from international buyers. Both cities attract part of the demand previously concentrated in London. Interest is strongest in the secondary market and in the segment of city residences.

Traditional resort destinations showed the most stable dynamics. Méribel grew by 9%, Marbella by 8.1%, remaining in demand as markets for family and generational residences. Demand here is supported not by short-term investment, but by long-term ownership and inheritance strategies.

Georgia: Development of Branded Hotel Formats

One of the key trends in the global luxury real estate market is the growth of serviced and branded formats. Buyers increasingly choose models with hotel infrastructure, luxury service standards, and centralized management.

This shift is gradually emerging in developing markets as well, including Georgia. A segment of branded hotel and residential projects is forming here, where returns depend on occupancy and the efficiency of operational management rather than individual rental activity.

At the local level, this model is still at an early stage. At the same time, investor interest is supported by relatively high returns from such assets and a more resilient business model compared to traditional rental properties. An additional driver is the growth in tourism and expanding international demand: in 2025, Georgia was visited by more than 7.8 million people, while international tourism revenues exceeded $4.69 billion, strengthening hotel occupancy and increasing the attractiveness of hospitality assets as an investment tool.

One of the most notable projects of this format is located in the Gonio resort area. The Wyndham Grand Batumi Gonio hotel complex has already, during the construction phase, been handed over to the international operator Aimbridge Hospitality, which is responsible for occupancy, pricing strategy, and operational efficiency.

Wyndham Grand belongs to the luxury segment of Wyndham Hotels & Resorts. There are only a limited number of such hotels worldwide, and only a few projects operate in an All Inclusive / Ultra All Inclusive format. Wyndham Grand Batumi Gonio is among them, highlighting its positioning in the upper segment.

In essence, this is not simply a real estate sale, but integration into an operating hotel system with an international brand and professional management. This is what sets such projects apart from the traditional apartment market and explains the growing investor interest in this format in Georgia.

What is changing in the global luxury housing market

Analysts at Knight Frank note that the prime segment remains resilient even under conditions of high inflation, expensive borrowing, and geopolitical tension. One of the main reasons remains the growth of private capital: an increasing number of wealthy buyers supports demand for luxury real estate in major cities and resort locations.

Tax policy and regulatory changes also have a significant impact. For some investors, the choice of country for residence or property purchase is increasingly determined not only by quality of life, but also by the level of fiscal burden.

Another key factor is the shortage of ready-to-move-in properties. Buyers in the upper segment prefer turnkey housing and are increasingly unwilling to invest in renovation or major repairs.

The branded residences market continues to expand. Knight Frank forecasts that the number of such projects worldwide will exceed 1,000 by 2030. The sector is gradually moving beyond traditional hotel partnerships, with standalone developments growing and new players emerging from fashion and wellness industries. Buyers are willing to pay not only for high-end housing, but also for curated living environments, guaranteed service levels, convenience, privacy, and high-quality infrastructure.