Вusiness / Real Estate / Investments / Analytics / Research / USA / United Kingdom / Germany / Netherlands / Japan / Poland / Slovakia 02.12.2025

Global real estate investment: key trends and Colliers’ outlook for 2026

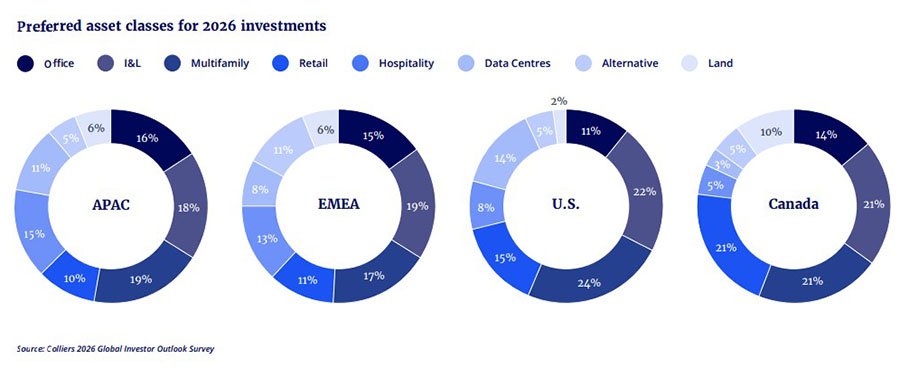

Colliers has released its Global Investor Outlook 2026, presenting new insights into capital movements across the global real estate market. The report highlights a sharp rise in the data-center segment, which attracted 31% of global fundraising, as well as the first signs of an office-market recovery. At the same time, regional investment flows have shifted: Europe and the Asia-Pacific region expanded their shares, while the United States saw its presence decline.

Office market: signs of recovery

After several years of declining activity, the office sector is beginning to rebound — a trend visible across multiple locations. In the Asia-Pacific region, investors are returning to assets in central business districts, with 68% of market participants focusing on them. Interest in more affordable business clusters is also strengthening: demand for offices in secondary hubs has risen by 18 percentage points over the year.

In Europe, large transactions exceeding £100 million are returning to the market. Deals of this scale have been rare in recent years, and their reappearance signals shifting sentiment among institutional investors.

In the United States, demand is moving toward high-quality office stock. New York, Los Angeles and Dallas remain the key markets where buyers are willing to work with assets capable of retaining tenants through upgraded infrastructure, prime locations and more stable income streams.

Logistics: demand for speed

The logistics real estate segment continues to show strong demand. In the Asia-Pacific region, large distribution centres dominate investor interest with a 27% share. They are followed by last-mile assets at 20% and light industrial properties at 19%. This balance reflects the combination of expanding e-commerce and heightened demand for fast delivery in major cities.

In Europe, the structure of demand is slightly different. While large warehouse complexes also account for 27%, last-mile assets represent 25%, and light industrial holds 14%. The most active markets are in Central and Eastern Europe — especially Poland and Slovakia — where the biggest recent portfolio deals have taken place. Land prices and rental rates remain noticeably lower than in Germany and the Netherlands, strengthening the region’s attractiveness.

In the United States, logistics has shifted from rapid expansion to a more stable phase. After a period of accelerated growth, rental rates are beginning to adjust, yet investor interest remains high. The strongest activity is recorded in Los Angeles, Dallas and Chicago — major hubs for distribution and storage that continue to support a steady flow of transactions.

Residential real estate: chronic undersupply

Housing remains one of the most resilient sectors, supported by limited supply and ongoing demand growth. In the Asia-Pacific region, 87% of investors focus primarily on the largest cities — Tokyo, Seoul and Sydney — where tenant concentration is high and the pace of new construction remains moderate.

In Europe, the priority remains on the multifamily rental market, a key destination for institutional capital. With a shortage of quality assets, the student housing segment is expanding rapidly, particularly in the UK, Spain, Germany and Italy. Transaction volumes are increasing most notably in cities with overloaded university infrastructure.

In North America, the dynamics differ by country. In Canada, investment in the residential sector rose by more than 20% in 2025 despite stricter immigration rules. In the US, investor interest is concentrated in Dallas, Los Angeles and Atlanta — major multifamily markets. Low levels of new construction in these cities are creating conditions for further rent growth in 2026.

Data centres: the new magnet for capital

The data-centre segment is showing the most rapid growth of all real estate asset classes. It accounts for 31% of global capital raised in the first three quarters of 2025, compared with around 15% in previous years. This surge is driven by the expansion of digital infrastructure and rising demand for computing capacity.

In the Asia-Pacific region, the strongest activity is seen in Australia, Japan and Singapore — markets with rapidly growing requirements for data-processing capacity. In the United States, investment is concentrated in Dallas, Northern Virginia and Phoenix, which are emerging as the main locations for new development.

The primary constraint on future growth is access to power. In Japan and India, electricity shortages are already delaying new projects, making the sector both promising and highly dependent on resources.

Capital reallocation and shifting strategies

By the third quarter of 2025, investment funds and asset managers had raised $165 billion — the same amount as in all of 2024. North America’s share of this capital decreased from 50% to 40%. Europe increased its fundraising volume by 50%, while the Asia-Pacific region (APAC) grew from 6% to 11%, a 130% jump. This shift shows that investors are moving away from narrow, single-market strategies toward broader, multi-country allocations, targeting locations where transactions are easier to structure and assets are more suitable for upgrading.

The growing interest in Europe and APAC is driven not only by relative returns but also by the ease of structuring transactions in these markets. At the same time, the US remains the largest market globally, yet its share of fundraising is decreasing for the first time in several years — a sign of shifting expectations and reassessed risk perceptions.

Deal structures are also changing. Investors are moving away from traditional funds, which receive only 9% of capital for core strategies, even though 37% of respondents list such strategies as preferred. Interest is rising in direct acquisitions, separate accounts and partnership structures in which investors take an equity stake in an asset or operating company and can influence its development strategy. These formats allow for faster deal execution and better alignment with tenant requirements.

Risks in 2026

Key risks identified by investors include rising construction costs, higher operating expenses, tariff-policy uncertainty and the possibility of corrections in financial markets. These factors may affect the timing of transactions and the availability of financing.

Colliers analysts also point to structural constraints. For data centres, the main issue is limited energy capacity, which in several countries is delaying the launch of new sites. In the office and residential sectors, maintenance and upgrade costs — including compliance with modern environmental standards — place significant pressure on asset performance.

Additional risks stem from permitting timelines and supply-chain delays. Even with stable demand, these factors can slow project delivery and reduce the appeal of certain markets. Nonetheless, the anticipated easing of monetary policy is expected to support a rise in transaction volumes in the first half of 2026.

Подсказки: real estate, investments, Colliers, 2026 forecast, data centers, logistics, housing, global market